Targa Resources Corp Earnings Summary

Targa Resources Corp. (NYSE: TRGP), a prominent player in the midstream services sector, reported their earnings for the fourth quarter and full-year 2024, showcasing a solid performance despite market challenges. For the fourth quarter, net income attributable to Targa rose to $351.0 million, marking an increase from the $299.6 million achieved in the same quarter of 2023. However, the full-year net income slipped slightly to $1,312.0 million from $1,345.9 million in 2023. NULLtheless, Targa demonstrated strong growth in adjusted EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization), reaching $1,122.2 million in the fourth quarter of 2024, up from $959.9 million in the previous year.

Targa Resources Corp Financial Results

The company's financial performance is detailed further in the table below:

| Financial Metric | Q4 2024 | Q4 2023 | FY 2024 | FY 2023 |

|---|---|---|---|---|

| Net Income ($M) | 351.0 | 299.6 | 1,312.0 | 1,345.9 |

| Adjusted EBITDA ($M) | 1,122.2 | 959.9 | 4,142.3 | 3,530.0 |

This earnings performance illustrates how Targa successfully managed to grow its adjusted EBITDA by 17% year-over-year, setting a record for 2024.

Revenue Breakdown

A key aspect of Targa’s operations lies in its diverse revenue streams, primarily derived from its Gathering and Processing (G&P) and Logistics and Transportation (L&T) segments. Their revenue performances are summarized in the following table:

| Segment | Q4 2024 Revenue ($M) | Performance Highlights |

|---|---|---|

| Gathering and Processing | Higher than Q4 2023 | Record Permian volumes |

| Logistics & Transportation | Higher than Q4 2023 | Record NGL volumes |

In-Depth Segment Analysis

1. Gathering and Processing Segment

Key drivers of the G&P segment revenue included increased natural gas inlet volumes and higher fees in the Permian Basin. Despite lower natural gas and condensate prices, the surge in production, facilitated by expanding infrastructure such as the Greenwood II and Bull Moose plants, bolstered this segment’s profitability.

2. Logistics and Transportation Segment

The L&T segment experienced notable growth due to increased pipeline transportation, fractionation, and LPG export volumes. Factors contributing to this growth included the operational start of the Daytona NGL Pipeline and the Train 10 fractionator. Additionally, marketing margins benefitted from favorable market conditions, enabling greater optimization opportunities.

Key Developments

Targa made significant strategic advancements during the quarter:

- Completed the Greenwood II and Train 10 fractionator projects.

- Initiated operations at the Bull Moose plant and a 800 MMcf/d front-end treater.

- Announced expansions such as the Delaware Express, Train 12 in Mont Belvieu, and increased LPG export capability at Galena Park Marine Terminal.

- Finalized a new $3.5 billion revolving credit facility to bolster liquidity.

- Refinanced preferred equity in Targa Badlands LLC, enhancing cost-effectiveness.

These developments, underpinned by robust operational execution, pave a pathway for continued growth.

Comments from Company Officers

Targa’s leadership celebrated the quarter’s achievements. They emphasized the operational and financial benefits realized through strategic capital investments and expansions, particularly in the Permian Basin, which continues to be a key growth driver. The expansions are expected to sustain Targa’s competitive position in the midstream sector.

Dividends and Share Repurchases

Targa announced a quarterly dividend of $0.75 per common share, translating to $3.00 on an annualized basis. For 2025, it plans to increase this to $4.00 per share annually. Additionally, Targa actively engaged in share repurchase activities, buying back approximately 610,683 shares in the fourth quarter of 2024 at an average price of $176.86, totaling $108.0 million. This effort reflects a strong commitment to return value to shareholders, with ample capacity remaining under their repurchase program.

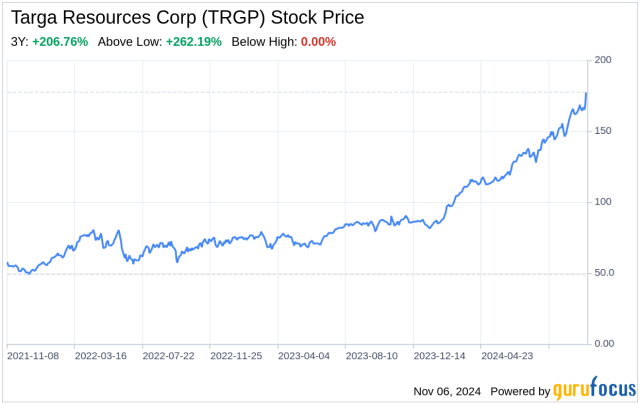

Targa Resources Corp Stock Forecast

Given Targa’s strong financial results and strategic expansions, the company's stock is poised for potential growth. While evaluating the forecast, it is essential to consider the positive momentum in adjusted EBITDA and strategic expansions over the next few years. With ongoing capital projects set to enhance infrastructure substantially, Targa’s stock could see its value exceed current levels. A high projection anticipates the stock price to rise significantly with increased volumes and efficiencies, while a lower projection would account for potential market volatilities and commodity price fluctuations.

Targa Resources Corp's robust financial performance, strategic expansions, and commitment to shareholder value position it as a formidable entity in the midstream sector, paving the way for growth and enhanced investor confidence.