EXPI Overview

-

$

0.000

0.000(0.000%)

At close0.000(0.000%)Aft-market

ET

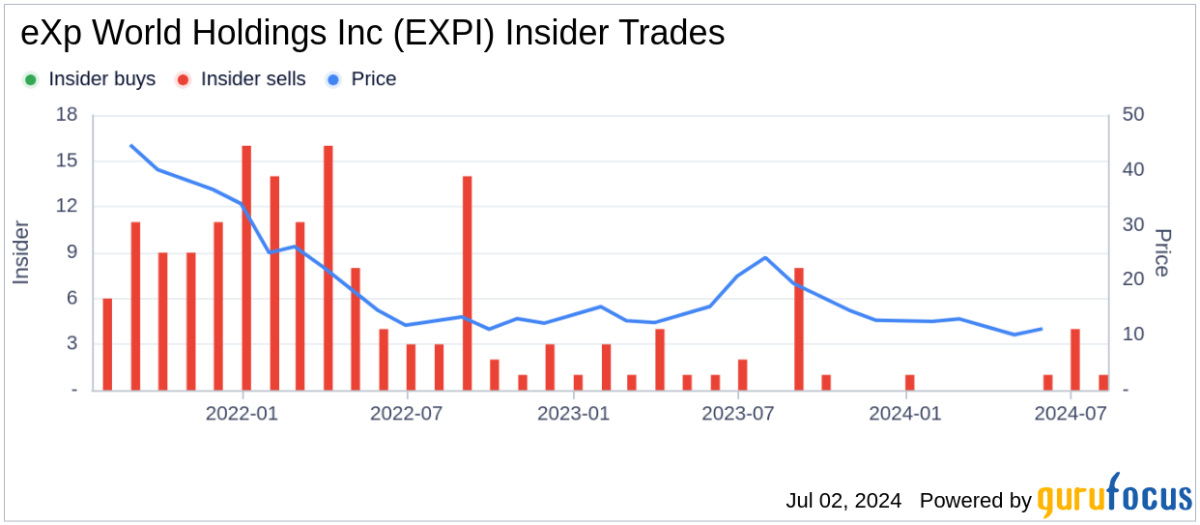

Loading chart...

The current price of EXPI is 0 USD — it has increased 0

eXp World Holdings, Inc. is the holding company for eXp Realty and SUCCESS Enterprises. eXp Realty is an independent real estate brokerage, with over 82,000 agents across 29 countries. eXp Realty also provides real estate agents commission splits, revenue share, equity ownership opportunities, and a global network that empowers agents to build businesses. SUCCESS Enterprises, anchored by SUCCESS magazine, provides personal and professional development. Its segments include North American Realty, International Realty and Other Affiliated Services. North American Realty segment includes real estate brokerage operations in the United States and Canada, as well as lead-generation and other real estate support services provided in North America. International Realty segment includes real estate brokerage operations in all other international locations. Other Affiliated Services segment includes its SUCCESS Magazine, and related media properties, which offer training, classes, and resources.

Wall Street analysts forecast EXPI stock price to rise over the next 12 months. According to Wall Street analysts, the average 1-year price target for EXPI is13.00 USD with a low forecast of 13.00 USD and a high forecast of 13.00 USD. However, analyst price targets are subjective and often lag stock prices, so investors should focus on the objective reasons behind analyst rating changes, which better reflect the company's fundamentals.

eXp World Holdings Inc revenue for the last quarter amounts to 1.01B USD, increased 1220.73

eXp World Holdings Inc. EPS for the last quarter amounts to -0.03 USD, decreased -57.14

eXp World Holdings Inc (EXPI) has 1834 emplpoyees as of June 24 2026.

Today EXPI has the market capitalization of 1.74B USD.