Tesla's Innovation and Investment Opportunities Amid High Valuation

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Feb 07 2026

0mins

Should l Buy TSLA?

Source: Fool

- CEO Influence: Tesla's CEO Elon Musk is a polarizing figure whose controversial statements and actions have led to increased stock volatility, prompting investors to carefully assess the associated risks before investing.

- High Valuation: With a current price-to-earnings ratio of 390, Tesla significantly exceeds its five-year average of 98 and the S&P 500's 28, indicating limited appeal for value investors and potential short-term investment risks.

- Business Diversification: Beyond electric vehicles, Tesla's involvement in battery storage, solar products, self-driving taxis, and humanoid robots showcases a diversification strategy that provides new growth drivers and investment opportunities for the company.

- Strategic Shift: Tesla's recent decision to discontinue slower-selling models X and S in favor of retooling plants for humanoid robot production signals a strategic expansion into robotics, which may benefit long-term investors if successful.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy TSLA?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

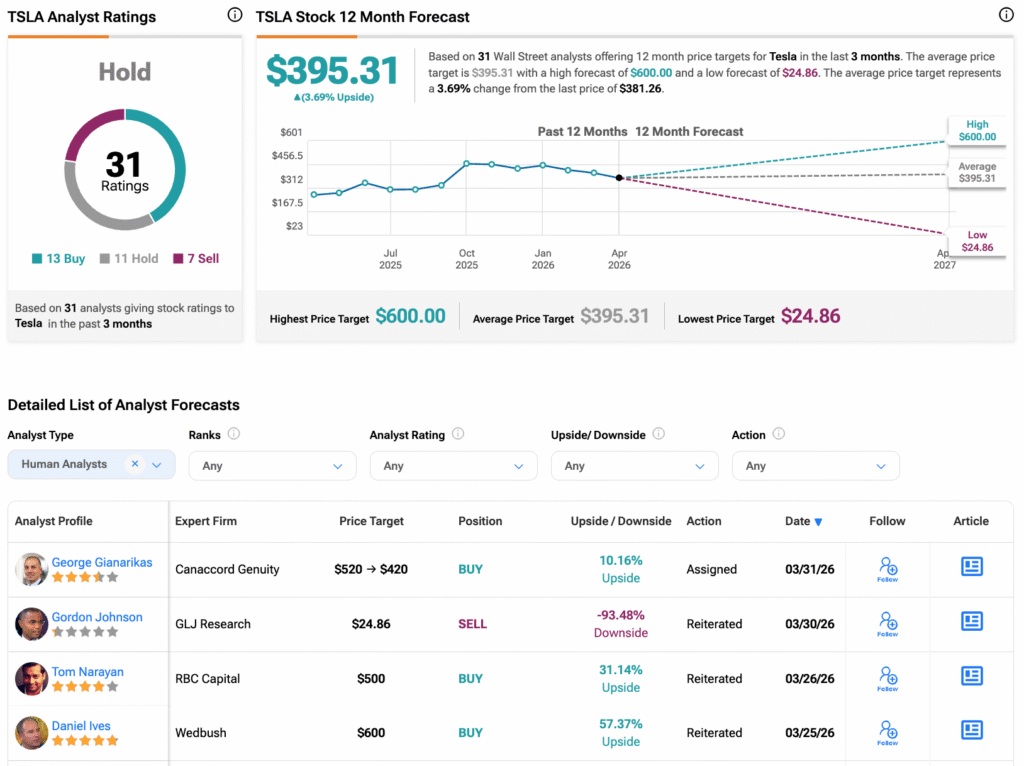

Analyst Views on TSLA

Wall Street analysts forecast TSLA stock price to rise

30 Analyst Rating

12 Buy

11 Hold

7 Sell

Hold

Current: 381.260

Low

25.28

Averages

401.93

High

600.00

Current: 381.260

Low

25.28

Averages

401.93

High

600.00

About TSLA

Tesla, Inc. designs, develops, manufactures, sells and leases high-performance fully electric vehicles and energy generation and storage systems, and offers services related to its products. Its segments include automotive, and energy generation and storage. The automotive segment includes the design, development, manufacturing, sales and leasing of high-performance fully electric vehicles, and sales of automotive regulatory credits. It also includes sales of used vehicles, non-warranty maintenance services and collisions, part sales, paid supercharging, insurance services revenue and retail merchandise sales. The energy generation and storage segment include the design, manufacture, installation, sales and leasing of solar energy generation and energy storage products and related services and sales of solar energy systems incentives. Its consumer vehicles include the Model 3, Y, S, X and Cybertruck. Its lithium-ion battery energy storage products include Powerwall and Megapack.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

SpaceX Files for IPO Targeting Over $1.75 Trillion Valuation

- IPO Overview: Billionaire Elon Musk's SpaceX has filed for an IPO with the U.S. SEC, targeting a valuation exceeding $1.75 trillion and aiming to raise up to $75 billion, potentially making it one of the largest public offerings in history if successful by June 2026.

- Tesla's Indirect Investment: Tesla has received government approval to convert its investment in Musk's xAI into a small stake in SpaceX, meaning Tesla shareholders will benefit indirectly from SpaceX's growth, with its value set to be publicly reflected in Tesla's assets post-IPO.

- Retail Investor Opportunities: SpaceX plans to allocate up to 30% of shares to retail investors, tripling the typical IPO norm, allowing Tesla's loyal retail investor base direct access from day one, enhancing their investment opportunities.

- Potential Merger Outlook: Wedbush analyst Dan Ives predicts a possible merger between Tesla and SpaceX as early as 2027, referring to this combination as the “holy grail” that could connect both disruptive tech companies within a single AI-driven ecosystem, showcasing significant strategic potential.

See More

Leasing Market Faces Challenges for EVs

- Leasing Market Risks: A wave of off-lease EVs is expected to return with values approximately $10,000 lower than projected, potentially costing the finance arms up to $8 billion, which could significantly impact overall industry profitability.

- Surge in Supply: By 2028, around 800,000 EVs are projected to hit the used market, leading to oversupply and further price depreciation, which may put additional financial strain on leasing companies.

- Tesla's Market Dominance: Tesla's leasing volume is substantial, with nearly 229,000 EVs leased last year, far exceeding the combined totals of General Motors and Ford, highlighting its strong influence in the industry.

- Financial Management Strategy: Despite industry challenges, Tesla mitigates its financial risk by managing a portion of its lease portfolio through partnerships with third-party lenders, allowing investors to remain cautiously optimistic while monitoring market developments in the coming years.

See More

Tesla Faces Off-Lease EV Depreciation Risks

- Leasing Market Risks: Tesla is expected to see a wave of off-lease EVs flooding the market in the coming years, with industry experts projecting these vehicles to return at values approximately $10,000 lower than anticipated, potentially costing the industry about $8 billion.

- Depreciation Trends: According to Cox Automotive, by 2025, a three-year-old EV will maintain only about 40% of its original value at auction, a significant drop from 90% in early 2022, indicating pressure on the used EV market.

- Tesla's Market Dominance: Tesla dominates the EV leasing market, having leased nearly 229,000 vehicles last year, which is significantly more than the combined total of General Motors and Ford, highlighting its strong industry influence.

- Investor Confidence Reminder: Despite the challenges posed by off-lease EV depreciation, Tesla's finance arm collaborates with third-party lenders, allowing it to mitigate most of the leasing losses, suggesting that investors need not panic just yet.

See More

Futures Drop as March Jobs Report Surprises

- Jobs Report Surprises: The March jobs report revealed significantly stronger job growth than anticipated, leading to increased investor concerns about an overheating economy, which triggered a decline in the futures market and affected overall market sentiment.

- Tesla's Stock Decline: Influenced by the overall market sentiment, Tesla's stock tumbled on Thursday, reflecting investor worries about overvalued tech stocks, which could lead to short-term capital outflows.

- Market Signal Analysis: The robust employment data may raise expectations for Federal Reserve interest rate hikes, prompting investors to monitor potential impacts of future monetary policy changes on the stock market, especially in a high-inflation environment.

- Investor Sentiment Fluctuation: While the strong jobs report bolstered confidence in economic recovery, it also raised concerns about a market correction, potentially leading to increased volatility in the short term.

See More

SpaceX Achieves Rocket Recovery, IPO on the Horizon

- Rocket Recovery Milestone: In October 2024, SpaceX successfully landed a previously launched rocket, marking a historic first that signifies a major breakthrough in aerospace technology, likely attracting increased investor interest in the space sector.

- Massive IPO Potential: SpaceX is projected to reach a valuation of $1.75 trillion, and if it goes public, it would become the largest IPO in market history, expected to have a profound impact on space-related stocks, similar to Tesla's influence on the electric vehicle market.

- Stock Price Surge: Following the news of SpaceX's impending IPO, stocks of companies like AST SpaceMobile, Rocket Lab, and Firefly Aerospace surged by 12%, 11.78%, and nearly 20% respectively, reflecting growing market confidence in the space economy.

- Reduced Launch Costs: SpaceX's reusable rocket technology is set to significantly lower launch costs, with traditional launches costing up to $1.5 billion compared to SpaceX's average of $62 million, and further reductions are anticipated, promoting sustainable growth in the aerospace industry.

See More

SpaceX IPO Set to Transform Space Economy

- IPO Buzz Ignites Market: SpaceX's impending IPO could value the company at $1.75 trillion, making it the largest IPO in market history, which is expected to instill confidence in space stocks similarly to how Tesla transformed the EV market.

- Space Stocks Surge: Following the IPO news, shares of AST SpaceMobile rose by 12%, Rocket Lab by 11.78%, and Firefly Aerospace by nearly 20%, reflecting a growing optimism and investment enthusiasm in the space sector.

- Significant Cost Reductions: SpaceX's reusable rocket technology has dramatically cut launch costs from approximately $2.1 billion for the Space Shuttle to around $62 million, with expectations for further reductions, enhancing the economic viability of space travel.

- Investment Opportunities in Smaller Firms: As SpaceX's IPO approaches, interest in smaller space companies is rising, encouraging investors to consider these firms ahead of the IPO to capitalize on the anticipated growth in the space economy.

See More

SpaceX Files for IPO Targeting Over $1.75 Trillion Valuation

- IPO Overview: Billionaire Elon Musk's SpaceX has filed for an IPO with the U.S. SEC, targeting a valuation exceeding $1.75 trillion and aiming to raise up to $75 billion, potentially making it one of the largest public offerings in history if successful by June 2026.

- Tesla's Indirect Investment: Tesla has received government approval to convert its investment in Musk's xAI into a small stake in SpaceX, meaning Tesla shareholders will benefit indirectly from SpaceX's growth, with its value set to be publicly reflected in Tesla's assets post-IPO.

- Retail Investor Opportunities: SpaceX plans to allocate up to 30% of shares to retail investors, tripling the typical IPO norm, allowing Tesla's loyal retail investor base direct access from day one, enhancing their investment opportunities.

- Potential Merger Outlook: Wedbush analyst Dan Ives predicts a possible merger between Tesla and SpaceX as early as 2027, referring to this combination as the “holy grail” that could connect both disruptive tech companies within a single AI-driven ecosystem, showcasing significant strategic potential.

See More

Leasing Market Faces Challenges for EVs

- Leasing Market Risks: A wave of off-lease EVs is expected to return with values approximately $10,000 lower than projected, potentially costing the finance arms up to $8 billion, which could significantly impact overall industry profitability.

- Surge in Supply: By 2028, around 800,000 EVs are projected to hit the used market, leading to oversupply and further price depreciation, which may put additional financial strain on leasing companies.

- Tesla's Market Dominance: Tesla's leasing volume is substantial, with nearly 229,000 EVs leased last year, far exceeding the combined totals of General Motors and Ford, highlighting its strong influence in the industry.

- Financial Management Strategy: Despite industry challenges, Tesla mitigates its financial risk by managing a portion of its lease portfolio through partnerships with third-party lenders, allowing investors to remain cautiously optimistic while monitoring market developments in the coming years.

See More

Tesla Faces Off-Lease EV Depreciation Risks

- Leasing Market Risks: Tesla is expected to see a wave of off-lease EVs flooding the market in the coming years, with industry experts projecting these vehicles to return at values approximately $10,000 lower than anticipated, potentially costing the industry about $8 billion.

- Depreciation Trends: According to Cox Automotive, by 2025, a three-year-old EV will maintain only about 40% of its original value at auction, a significant drop from 90% in early 2022, indicating pressure on the used EV market.

- Tesla's Market Dominance: Tesla dominates the EV leasing market, having leased nearly 229,000 vehicles last year, which is significantly more than the combined total of General Motors and Ford, highlighting its strong industry influence.

- Investor Confidence Reminder: Despite the challenges posed by off-lease EV depreciation, Tesla's finance arm collaborates with third-party lenders, allowing it to mitigate most of the leasing losses, suggesting that investors need not panic just yet.

See More

Futures Drop as March Jobs Report Surprises

- Jobs Report Surprises: The March jobs report revealed significantly stronger job growth than anticipated, leading to increased investor concerns about an overheating economy, which triggered a decline in the futures market and affected overall market sentiment.

- Tesla's Stock Decline: Influenced by the overall market sentiment, Tesla's stock tumbled on Thursday, reflecting investor worries about overvalued tech stocks, which could lead to short-term capital outflows.

- Market Signal Analysis: The robust employment data may raise expectations for Federal Reserve interest rate hikes, prompting investors to monitor potential impacts of future monetary policy changes on the stock market, especially in a high-inflation environment.

- Investor Sentiment Fluctuation: While the strong jobs report bolstered confidence in economic recovery, it also raised concerns about a market correction, potentially leading to increased volatility in the short term.

See More

SpaceX Achieves Rocket Recovery, IPO on the Horizon

- Rocket Recovery Milestone: In October 2024, SpaceX successfully landed a previously launched rocket, marking a historic first that signifies a major breakthrough in aerospace technology, likely attracting increased investor interest in the space sector.

- Massive IPO Potential: SpaceX is projected to reach a valuation of $1.75 trillion, and if it goes public, it would become the largest IPO in market history, expected to have a profound impact on space-related stocks, similar to Tesla's influence on the electric vehicle market.

- Stock Price Surge: Following the news of SpaceX's impending IPO, stocks of companies like AST SpaceMobile, Rocket Lab, and Firefly Aerospace surged by 12%, 11.78%, and nearly 20% respectively, reflecting growing market confidence in the space economy.

- Reduced Launch Costs: SpaceX's reusable rocket technology is set to significantly lower launch costs, with traditional launches costing up to $1.5 billion compared to SpaceX's average of $62 million, and further reductions are anticipated, promoting sustainable growth in the aerospace industry.

See More

SpaceX IPO Set to Transform Space Economy

- IPO Buzz Ignites Market: SpaceX's impending IPO could value the company at $1.75 trillion, making it the largest IPO in market history, which is expected to instill confidence in space stocks similarly to how Tesla transformed the EV market.

- Space Stocks Surge: Following the IPO news, shares of AST SpaceMobile rose by 12%, Rocket Lab by 11.78%, and Firefly Aerospace by nearly 20%, reflecting a growing optimism and investment enthusiasm in the space sector.

- Significant Cost Reductions: SpaceX's reusable rocket technology has dramatically cut launch costs from approximately $2.1 billion for the Space Shuttle to around $62 million, with expectations for further reductions, enhancing the economic viability of space travel.

- Investment Opportunities in Smaller Firms: As SpaceX's IPO approaches, interest in smaller space companies is rising, encouraging investors to consider these firms ahead of the IPO to capitalize on the anticipated growth in the space economy.

See More