Kiniksa Pharmaceuticals Q1 Earnings Exceed Expectations

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Apr 28 2026

0mins

Source: seekingalpha

- Earnings Beat: Kiniksa Pharmaceuticals reported a Q1 GAAP EPS of $0.27, exceeding expectations by $0.09, indicating a robust enhancement in profitability and competitive positioning in the market.

- Significant Revenue Growth: The company achieved Q1 revenue of $214.3 million, reflecting a 55.6% year-over-year increase and surpassing expectations by $8.21 million, demonstrating strong product demand and market acceptance.

- Future Revenue Guidance: Kiniksa anticipates 2026 ARCALYST net product revenue between $930 million and $945 million, an increase from the previous guidance of $900 million to $920 million, showcasing confidence in future market potential.

- Positive Cash Flow: The company expects its current operating plan to remain cash flow positive on an annual basis, indicating effective financial management and resource allocation that will support future growth strategies.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy KNSA?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on KNSA

Wall Street analysts forecast KNSA stock price to rise

6 Analyst Rating

6 Buy

0 Hold

0 Sell

Strong Buy

Current: 50.840

Low

48.00

Averages

53.50

High

60.00

Current: 50.840

Low

48.00

Averages

53.50

High

60.00

About KNSA

Kiniksa Pharmaceuticals International, plc is a biopharmaceutical company focused on discovering, acquiring, developing and commercializing novel therapies for diseases with unmet need, with a focus on cardiovascular indications. Its portfolio of assets is based on strong biologic rationale or validated mechanisms and offers the potential for differentiation. Its ARCALYST is used for the treatment of recurrent pericarditis and reduces the risk of recurrence in adults and children 12 years and older. ARCALYST is also approved for the treatment of Cryopyrin-Associated Periodic Syndromes (CAPS), including Familial Cold Autoinflammatory Syndrome (FCAS) and Muckle-Wells Syndrome, and the maintenance of remission in Deficiency of Interleukin-1 Receptor Antagonist. Its other portfolio includes KPL-387, KPL-1161, Abiprubart, and Mavrilimumab. Mavrilimumab is an investigational monoclonal antibody inhibitor targeting granulocyte-macrophage colony stimulating factor receptor alpha.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Kiniksa Pharmaceuticals to Participate in Investor Conferences

- Investor Conference Schedule: Kiniksa Pharmaceuticals will participate in two significant investor conferences in June 2026, specifically the Jefferies Global Healthcare Conference on June 3 and the Goldman Sachs 47th Annual Global Healthcare Conference on June 9, showcasing its latest advancements in the biopharmaceutical sector.

- Live Webcast Availability: The company will provide live webcasts of the presentations through the Investors & Media section of its website, ensuring that investors can access real-time information, with replays available within 48 hours post-event, enhancing transparency and information accessibility.

- Company Mission and Vision: Kiniksa is dedicated to improving patients' lives by discovering, acquiring, developing, and commercializing novel therapies, particularly focusing on cardiovascular indications, highlighting its strategic positioning in addressing unmet medical needs.

- Biopharmaceutical Market Potential: Kiniksa's portfolio is based on strong biological rationale or validated mechanisms, offering differentiation potential, indicating the company's commitment to innovation and growth in the competitive biopharmaceutical market.

See More

Kiniksa Pharmaceuticals International (KNSA.US) Officer Plans to Sell $3.14 Million in Common Stock via Form 144

Stock Sale Announcement: Paolini John F. intends to sell 58,424 shares of Kiniksa Pharmaceuticals International on May 1, with a total market value of approximately $3.14 million.

Reduction in Shareholding: Since March 2, 2026, Paolini John F. has reduced his shareholding in Kiniksa Pharmaceuticals International by 40,000 shares, valued at around $1.79 million.

See More

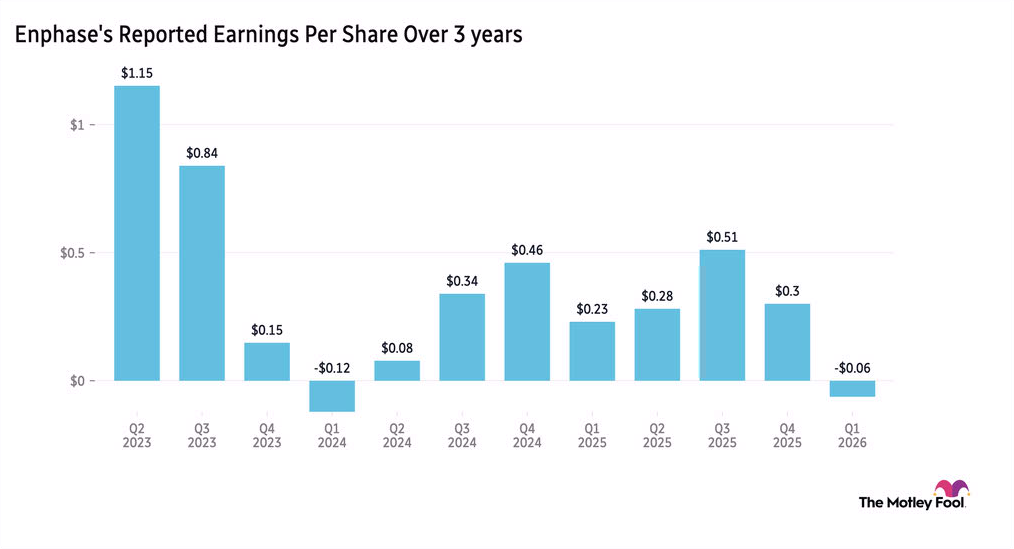

Enphase Energy Drops as Solar Demand Weakens

- Earnings Decline: Enphase Energy reported a 31% year-over-year drop in non-GAAP earnings per share for Q1, leading to a more than 10% decline in pre-market trading, highlighting significant challenges in the U.S. market amid tariff costs and oil-centric energy policies.

- International Market Expansion: Despite domestic struggles, CEO Kothandaraman noted healthy double-digit growth in battery demand across Europe, which is expected to drive revenue growth; however, to combat competition, the company plans to reduce distributor prices for batteries by approximately 10% in May.

- Revenue Outlook: Management anticipates Q2 revenue between $280 million and $310 million, following Q1 revenue of $282.9 million, while maintaining non-GAAP gross margins between 44% and 47%, indicating confidence in the commercialization of next-generation products.

- Intensifying Market Competition: With a prior 20% price reduction on microinverters implemented last December, the upcoming price adjustments may impact short-term margins but could pave the way for long-term market share gains, reflecting the company's adaptability in the rapidly evolving solar market.

See More

Kiniksa Pharmaceuticals Reports Strong Q1 Earnings, Shares Surge

- Strong Performance: Kiniksa Pharmaceuticals' inaugural Q1 earnings report for 2026 revealed revenue exceeding $214 million, a significant increase from last year's under $138 million, convincingly beating analyst expectations of $207 million, showcasing the company's robust performance in the biotech sector.

- Net Income Doubles: Under GAAP, Kiniksa's net income more than doubled from $8.5 million in Q1 2025 to $22.6 million, with earnings per share reaching $0.27, significantly surpassing the analyst forecast of $0.21, reflecting a marked improvement in the company's profitability.

- Product Success Drives Growth: The recent approval of Arcalyst, particularly for the heart condition pericarditis, has been a key driver of Kiniksa's popularity, prompting management to raise its 2026 net sales forecast to between $930 million and $945 million, indicating strong market demand for the drug.

- Positive Market Reaction: Following the earnings release, Kiniksa's stock surged nearly 24%, bringing its market capitalization to $3.3 billion, demonstrating investor confidence in the company's future growth potential, especially regarding the development of multiple indications for its single product.

See More

Kiniksa Pharmaceuticals Reports Strong Sales Growth

- Sales Performance Surge: Kiniksa Pharmaceuticals reported first-quarter sales of over $214 million for its drug Arcalyst, marking a significant increase from last year's $138 million, indicating strong market demand and product acceptance.

- Net Income Doubling: Under GAAP, Kiniksa's net income more than doubled from $8.5 million in Q1 2025 to $22.6 million ($0.27 per share), surpassing analyst expectations of $0.21, reflecting a notable improvement in profitability.

- Sales Forecast Upgrade: Management raised the 2026 net sales guidance for Arcalyst from $900 million to $920 million to a new range of $930 million to $945 million, demonstrating confidence in the drug's market potential following its recent approval for heart disorder pericarditis.

- Positive Market Reaction: Following the release of its inaugural 2026 earnings report, Kiniksa's stock surged nearly 24% during the trading session, showcasing strong investor confidence in the company's growth prospects and further solidifying its position in the biotech sector.

See More

Kiniksa Pharmaceuticals Q1 2026 Earnings Call Highlights

- Significant Sales Growth: Kiniksa Pharmaceuticals reported Q1 2026 ARCALYST sales of $214.3 million, reflecting a 56% year-over-year increase, indicating a growing market acceptance that is expected to further drive overall revenue growth.

- Revenue Guidance Raised: The company has raised its full-year 2026 revenue guidance from $900 million to $920 million to a new range of $930 million to $945 million, reflecting management's confidence in future performance, particularly with the increase in new prescribers.

- Strong Cash Flow: Net income surged to $22.6 million in Q1, with a cash balance of $468.1 million, demonstrating the company's ability to maintain positive cash flow while continuing to invest in R&D, thereby enhancing its financial stability.

- New Marketing Initiatives: Kiniksa launched a direct-to-consumer campaign called “Heart's Home” aimed at increasing patient awareness of ARCALYST, especially given that only 14% of recurrent pericarditis patients are currently aware of the drug, which will help expand market share.

See More

Kiniksa Pharmaceuticals to Participate in Investor Conferences

- Investor Conference Schedule: Kiniksa Pharmaceuticals will participate in two significant investor conferences in June 2026, specifically the Jefferies Global Healthcare Conference on June 3 and the Goldman Sachs 47th Annual Global Healthcare Conference on June 9, showcasing its latest advancements in the biopharmaceutical sector.

- Live Webcast Availability: The company will provide live webcasts of the presentations through the Investors & Media section of its website, ensuring that investors can access real-time information, with replays available within 48 hours post-event, enhancing transparency and information accessibility.

- Company Mission and Vision: Kiniksa is dedicated to improving patients' lives by discovering, acquiring, developing, and commercializing novel therapies, particularly focusing on cardiovascular indications, highlighting its strategic positioning in addressing unmet medical needs.

- Biopharmaceutical Market Potential: Kiniksa's portfolio is based on strong biological rationale or validated mechanisms, offering differentiation potential, indicating the company's commitment to innovation and growth in the competitive biopharmaceutical market.

See More

Kiniksa Pharmaceuticals International (KNSA.US) Officer Plans to Sell $3.14 Million in Common Stock via Form 144

Stock Sale Announcement: Paolini John F. intends to sell 58,424 shares of Kiniksa Pharmaceuticals International on May 1, with a total market value of approximately $3.14 million.

Reduction in Shareholding: Since March 2, 2026, Paolini John F. has reduced his shareholding in Kiniksa Pharmaceuticals International by 40,000 shares, valued at around $1.79 million.

See More

Enphase Energy Drops as Solar Demand Weakens

- Earnings Decline: Enphase Energy reported a 31% year-over-year drop in non-GAAP earnings per share for Q1, leading to a more than 10% decline in pre-market trading, highlighting significant challenges in the U.S. market amid tariff costs and oil-centric energy policies.

- International Market Expansion: Despite domestic struggles, CEO Kothandaraman noted healthy double-digit growth in battery demand across Europe, which is expected to drive revenue growth; however, to combat competition, the company plans to reduce distributor prices for batteries by approximately 10% in May.

- Revenue Outlook: Management anticipates Q2 revenue between $280 million and $310 million, following Q1 revenue of $282.9 million, while maintaining non-GAAP gross margins between 44% and 47%, indicating confidence in the commercialization of next-generation products.

- Intensifying Market Competition: With a prior 20% price reduction on microinverters implemented last December, the upcoming price adjustments may impact short-term margins but could pave the way for long-term market share gains, reflecting the company's adaptability in the rapidly evolving solar market.

See More

Kiniksa Pharmaceuticals Reports Strong Q1 Earnings, Shares Surge

- Strong Performance: Kiniksa Pharmaceuticals' inaugural Q1 earnings report for 2026 revealed revenue exceeding $214 million, a significant increase from last year's under $138 million, convincingly beating analyst expectations of $207 million, showcasing the company's robust performance in the biotech sector.

- Net Income Doubles: Under GAAP, Kiniksa's net income more than doubled from $8.5 million in Q1 2025 to $22.6 million, with earnings per share reaching $0.27, significantly surpassing the analyst forecast of $0.21, reflecting a marked improvement in the company's profitability.

- Product Success Drives Growth: The recent approval of Arcalyst, particularly for the heart condition pericarditis, has been a key driver of Kiniksa's popularity, prompting management to raise its 2026 net sales forecast to between $930 million and $945 million, indicating strong market demand for the drug.

- Positive Market Reaction: Following the earnings release, Kiniksa's stock surged nearly 24%, bringing its market capitalization to $3.3 billion, demonstrating investor confidence in the company's future growth potential, especially regarding the development of multiple indications for its single product.

See More

Kiniksa Pharmaceuticals Reports Strong Sales Growth

- Sales Performance Surge: Kiniksa Pharmaceuticals reported first-quarter sales of over $214 million for its drug Arcalyst, marking a significant increase from last year's $138 million, indicating strong market demand and product acceptance.

- Net Income Doubling: Under GAAP, Kiniksa's net income more than doubled from $8.5 million in Q1 2025 to $22.6 million ($0.27 per share), surpassing analyst expectations of $0.21, reflecting a notable improvement in profitability.

- Sales Forecast Upgrade: Management raised the 2026 net sales guidance for Arcalyst from $900 million to $920 million to a new range of $930 million to $945 million, demonstrating confidence in the drug's market potential following its recent approval for heart disorder pericarditis.

- Positive Market Reaction: Following the release of its inaugural 2026 earnings report, Kiniksa's stock surged nearly 24% during the trading session, showcasing strong investor confidence in the company's growth prospects and further solidifying its position in the biotech sector.

See More

Kiniksa Pharmaceuticals Q1 2026 Earnings Call Highlights

- Significant Sales Growth: Kiniksa Pharmaceuticals reported Q1 2026 ARCALYST sales of $214.3 million, reflecting a 56% year-over-year increase, indicating a growing market acceptance that is expected to further drive overall revenue growth.

- Revenue Guidance Raised: The company has raised its full-year 2026 revenue guidance from $900 million to $920 million to a new range of $930 million to $945 million, reflecting management's confidence in future performance, particularly with the increase in new prescribers.

- Strong Cash Flow: Net income surged to $22.6 million in Q1, with a cash balance of $468.1 million, demonstrating the company's ability to maintain positive cash flow while continuing to invest in R&D, thereby enhancing its financial stability.

- New Marketing Initiatives: Kiniksa launched a direct-to-consumer campaign called “Heart's Home” aimed at increasing patient awareness of ARCALYST, especially given that only 14% of recurrent pericarditis patients are currently aware of the drug, which will help expand market share.

See More