Iridium Communications Set to Announce Q1 Earnings on April 23

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Apr 22 2026

0mins

Source: seekingalpha

- Earnings Announcement: Iridium Communications is set to release its Q1 2023 earnings report on April 23 before market open, with consensus estimates predicting an EPS of $0.28 and revenue of $219.18 million, reflecting a 2% year-over-year growth.

- Performance Analysis: Over the past year, Iridium has exceeded EPS estimates 25% of the time and revenue estimates 50% of the time, indicating volatility in its profitability metrics.

- Estimate Revisions: In the last three months, there have been no upward revisions to EPS estimates, with one downward revision, while revenue estimates saw one upward and two downward revisions, suggesting a cautious market outlook on the company's performance.

- Future Growth Target: Iridium has set a pro forma free cash flow target of $318 million by 2026, indicating confidence in future growth driven by new technologies and partnerships despite current market challenges.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy IRDM?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on IRDM

Wall Street analysts forecast IRDM stock price to fall

7 Analyst Rating

4 Buy

2 Hold

1 Sell

Moderate Buy

Current: 51.260

Low

16.00

Averages

25.83

High

37.00

Current: 51.260

Low

16.00

Averages

25.83

High

37.00

About IRDM

Iridium Communications Inc. is a provider of global voice, data, and positioning, navigation and timing (PNT) satellite services. The Company is a commercial provider of communications services offering true global coverage, connecting people, organizations and assets to and from anywhere, in real time. Its principal vertical lines of business include land mobile, maritime, aviation, Internet of things (IoT), hosted payloads and other data services, which includes navigation and timing (PNT), and the United States government. Its handset offerings include Iridium 9555, Iridium Extreme, Iridium Extreme PTT, Iridium GO!, and Iridium GO! Exec. The Company's primary business is to provide voice and data communications services to businesses, the United States and foreign governments, non-governmental organizations, and consumers via our satellite network, which has an architecture of over 66 operational satellites with in-orbit spares and related ground infrastructure.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

AST SpaceMobile Shares Drop 14.79% Amid Launch Concerns

- Significant Stock Decline: AST SpaceMobile's shares closed at $113.41 on Friday, down 14.79%, primarily due to the explosion of Blue Origin's New Glenn rocket and a downgrade from Deutsche Bank, indicating heightened market concerns over the company's execution risks.

- Surge in Trading Volume: The trading volume reached 54.8 million shares, which is 159% above the three-month average, reflecting intense investor interest and significant volatility in market sentiment regarding the company's future.

- Launch Plan Risks: AST SpaceMobile aims to launch approximately 45 satellites this year; however, delays from Blue Origin could jeopardize the deployment of its BlueBird constellation, adding uncertainty to the company's growth trajectory and investor confidence.

- Impact of Downgrade: Deutsche Bank cut AST SpaceMobile's price target to $106, amplifying investor concerns, and as a speculative space venture, the company is expected to experience increased market volatility moving forward.

See More

SpaceX's Starlink Business Sees Significant Growth

- Significant Revenue Growth: SpaceX's Starlink generated $11.39 billion in revenue last year, accounting for 61% of total sales, with this figure rising to 69% in Q1 of this year, underscoring its critical role in the company's overall performance.

- Strong Profitability: Starlink was the only profitable division for SpaceX, generating $4.42 billion in net income last year, while the rocket launch division lost $657 million and the AI division incurred a $6.35 billion deficit, highlighting Starlink's strategic importance as a profit engine.

- Rapid User Base Expansion: Starlink's user base surpassed 10.3 million in Q1, more than doubling from the previous year, indicating strong global demand, particularly among commercial clients such as airlines, enhancing its market position.

- Surge in Capital Expenditures: SpaceX reported capital expenditures of $10.1 billion in Q1, more than doubling year-over-year, with $7.7 billion allocated to AI development, reflecting the company's strategic investment in technology innovation and market competitiveness.

See More

Iridium Communications Approves Updated Employee Equity Plan and Dividend

- Updated Employee Equity Plan: At its annual meeting, Iridium Communications approved a revised 2015 Equity Incentive Plan allowing for the issuance of up to 42.9 million shares for future stock-based compensation, which will enhance employee motivation and attract talent, thereby driving long-term growth for the company.

- Board Re-election: Shareholders voted unanimously to reelect all 11 board members for terms through 2027, indicating strong investor confidence in the company's governance structure, which helps maintain management stability and strategic alignment.

- Quarterly Cash Dividend: Iridium announced a quarterly cash dividend of $0.15 per share, scheduled for payment on June 30, which not only provides stable returns to shareholders but may also attract more investors to the company's long-term value proposition.

- Aireon Acquisition Progress: Iridium plans to acquire the remaining 61% stake in Aireon for approximately $366.7 million, which is expected to contribute around $100 million in annual revenue and $30 million in operational EBITDA, further solidifying its control over the aviation data network.

See More

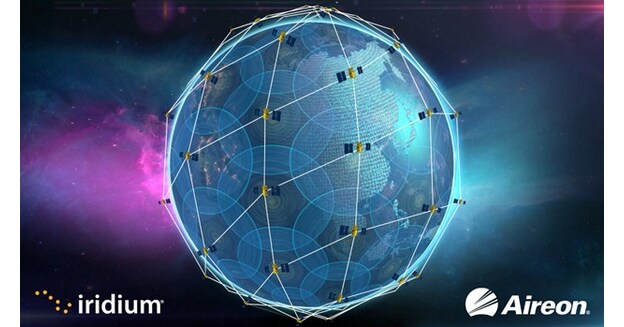

Iridium Communications to Acquire Remaining 61% of Aireon for $366.7M

- Acquisition Overview: Iridium Communications has agreed to acquire the remaining 61% equity interests of Aireon for approximately $366.7 million, with 50% of the purchase price paid at closing and the remaining 50% due one year later, reflecting the company's confidence in future growth.

- Debt Assumption: Iridium will assume Aireon's outstanding debt of about $155 million, indicating a comprehensive approach to the acquisition that prioritizes overall financial health, with plans to fund the purchase through current liquidity and future cash from operations.

- Revenue Growth Expectations: Aireon's total revenue has grown at a compound annual growth rate of 10% over the past three years, and Iridium anticipates that the acquisition will generate at least an additional $100 million in service revenue and $30 million in OEBITDA annually, enhancing its competitive position.

- Strategic Implications: This acquisition will enable Iridium to capture a larger market share in the world's only space-based Automatic Dependent Surveillance-Broadcast (ADS-B) air traffic surveillance system, which is expected to drive future growth and profitability for the company.

See More

Iridium Acquires Aireon to Enhance Aviation Safety

- Acquisition Overview: Iridium Communications announced the acquisition of Aireon LLC for approximately $366.7 million, which operates the world's only space-based air traffic surveillance system, enhancing Iridium's strategic position in aviation safety.

- Market Impact: The acquisition is expected to add at least $100 million in service revenue and $30 million in OEBITDA annually, reflecting Aireon's 10% compound annual growth rate over the past three years, further solidifying Iridium's market leadership.

- Technological Integration Benefits: By integrating Aireon's surveillance and data services with Iridium's global satellite communication network, Iridium will provide four critical aviation capabilities, including GPS jamming detection, thereby enhancing global aviation safety and efficiency.

- Future Development Potential: This transaction positions Iridium to develop new technologies such as space-based VHF communications, driving innovation and growth in the aviation industry, ensuring a competitive edge in the face of increasing air traffic.

See More

FCC Rejects Expansion of Satellite Spectrum Access

- FCC Decision Impacts Market: The FCC's rejection of requests from satellite operators, including AST SpaceMobile, to expand access to the 1.5 GHz and 2 GHz bands confirms existing control, limiting AST's expansion plans and potentially diminishing its competitive edge in the market.

- Stock Price Decline: AST SpaceMobile's shares have dropped 8% this week, closing at $78.75 on Thursday, reflecting cautious investor sentiment in response to the FCC ruling, particularly as competition with SpaceX and Amazon intensifies.

- Satellite Launch Progress: Despite FCC restrictions, AST SpaceMobile continues to advance its next-generation satellites, with BlueBird-8 through BlueBird-10 expected to be ready for shipment within 30 days, demonstrating the company's ongoing commitment to technological development.

- Mixed Investor Sentiment: While retail sentiment for ASTS remains bullish, concerns about the stock price persist, with users on social media expressing disappointment over the lack of a clear launch schedule, which could impact future investment decisions.

See More

AST SpaceMobile Shares Drop 14.79% Amid Launch Concerns

- Significant Stock Decline: AST SpaceMobile's shares closed at $113.41 on Friday, down 14.79%, primarily due to the explosion of Blue Origin's New Glenn rocket and a downgrade from Deutsche Bank, indicating heightened market concerns over the company's execution risks.

- Surge in Trading Volume: The trading volume reached 54.8 million shares, which is 159% above the three-month average, reflecting intense investor interest and significant volatility in market sentiment regarding the company's future.

- Launch Plan Risks: AST SpaceMobile aims to launch approximately 45 satellites this year; however, delays from Blue Origin could jeopardize the deployment of its BlueBird constellation, adding uncertainty to the company's growth trajectory and investor confidence.

- Impact of Downgrade: Deutsche Bank cut AST SpaceMobile's price target to $106, amplifying investor concerns, and as a speculative space venture, the company is expected to experience increased market volatility moving forward.

See More

SpaceX's Starlink Business Sees Significant Growth

- Significant Revenue Growth: SpaceX's Starlink generated $11.39 billion in revenue last year, accounting for 61% of total sales, with this figure rising to 69% in Q1 of this year, underscoring its critical role in the company's overall performance.

- Strong Profitability: Starlink was the only profitable division for SpaceX, generating $4.42 billion in net income last year, while the rocket launch division lost $657 million and the AI division incurred a $6.35 billion deficit, highlighting Starlink's strategic importance as a profit engine.

- Rapid User Base Expansion: Starlink's user base surpassed 10.3 million in Q1, more than doubling from the previous year, indicating strong global demand, particularly among commercial clients such as airlines, enhancing its market position.

- Surge in Capital Expenditures: SpaceX reported capital expenditures of $10.1 billion in Q1, more than doubling year-over-year, with $7.7 billion allocated to AI development, reflecting the company's strategic investment in technology innovation and market competitiveness.

See More

Iridium Communications Approves Updated Employee Equity Plan and Dividend

- Updated Employee Equity Plan: At its annual meeting, Iridium Communications approved a revised 2015 Equity Incentive Plan allowing for the issuance of up to 42.9 million shares for future stock-based compensation, which will enhance employee motivation and attract talent, thereby driving long-term growth for the company.

- Board Re-election: Shareholders voted unanimously to reelect all 11 board members for terms through 2027, indicating strong investor confidence in the company's governance structure, which helps maintain management stability and strategic alignment.

- Quarterly Cash Dividend: Iridium announced a quarterly cash dividend of $0.15 per share, scheduled for payment on June 30, which not only provides stable returns to shareholders but may also attract more investors to the company's long-term value proposition.

- Aireon Acquisition Progress: Iridium plans to acquire the remaining 61% stake in Aireon for approximately $366.7 million, which is expected to contribute around $100 million in annual revenue and $30 million in operational EBITDA, further solidifying its control over the aviation data network.

See More

Iridium Communications to Acquire Remaining 61% of Aireon for $366.7M

- Acquisition Overview: Iridium Communications has agreed to acquire the remaining 61% equity interests of Aireon for approximately $366.7 million, with 50% of the purchase price paid at closing and the remaining 50% due one year later, reflecting the company's confidence in future growth.

- Debt Assumption: Iridium will assume Aireon's outstanding debt of about $155 million, indicating a comprehensive approach to the acquisition that prioritizes overall financial health, with plans to fund the purchase through current liquidity and future cash from operations.

- Revenue Growth Expectations: Aireon's total revenue has grown at a compound annual growth rate of 10% over the past three years, and Iridium anticipates that the acquisition will generate at least an additional $100 million in service revenue and $30 million in OEBITDA annually, enhancing its competitive position.

- Strategic Implications: This acquisition will enable Iridium to capture a larger market share in the world's only space-based Automatic Dependent Surveillance-Broadcast (ADS-B) air traffic surveillance system, which is expected to drive future growth and profitability for the company.

See More

Iridium Acquires Aireon to Enhance Aviation Safety

- Acquisition Overview: Iridium Communications announced the acquisition of Aireon LLC for approximately $366.7 million, which operates the world's only space-based air traffic surveillance system, enhancing Iridium's strategic position in aviation safety.

- Market Impact: The acquisition is expected to add at least $100 million in service revenue and $30 million in OEBITDA annually, reflecting Aireon's 10% compound annual growth rate over the past three years, further solidifying Iridium's market leadership.

- Technological Integration Benefits: By integrating Aireon's surveillance and data services with Iridium's global satellite communication network, Iridium will provide four critical aviation capabilities, including GPS jamming detection, thereby enhancing global aviation safety and efficiency.

- Future Development Potential: This transaction positions Iridium to develop new technologies such as space-based VHF communications, driving innovation and growth in the aviation industry, ensuring a competitive edge in the face of increasing air traffic.

See More

FCC Rejects Expansion of Satellite Spectrum Access

- FCC Decision Impacts Market: The FCC's rejection of requests from satellite operators, including AST SpaceMobile, to expand access to the 1.5 GHz and 2 GHz bands confirms existing control, limiting AST's expansion plans and potentially diminishing its competitive edge in the market.

- Stock Price Decline: AST SpaceMobile's shares have dropped 8% this week, closing at $78.75 on Thursday, reflecting cautious investor sentiment in response to the FCC ruling, particularly as competition with SpaceX and Amazon intensifies.

- Satellite Launch Progress: Despite FCC restrictions, AST SpaceMobile continues to advance its next-generation satellites, with BlueBird-8 through BlueBird-10 expected to be ready for shipment within 30 days, demonstrating the company's ongoing commitment to technological development.

- Mixed Investor Sentiment: While retail sentiment for ASTS remains bullish, concerns about the stock price persist, with users on social media expressing disappointment over the lack of a clear launch schedule, which could impact future investment decisions.

See More