Instacart Surpasses Q4 Estimates with Strong Guidance

- Strong Performance: Instacart reported better-than-expected fourth-quarter revenue with gross transaction value (GTV) growing 14%, marking its strongest quarterly growth in three years, indicating robust growth potential in a competitive market.

- Record Order Volume: Total orders reached 89.5 million, surpassing the StreetAccount estimate of 87.8 million, demonstrating Instacart's success in attracting customers and further solidifying its market position.

- Optimistic Guidance: The company forecasts GTV between $10.13 billion and $10.28 billion, significantly above the $9.97 billion estimate, reflecting management's confidence in future growth.

- Technology Investment Drive: Instacart is actively investing in new technologies and AI tools to enhance customer engagement and attract more users, with the CEO stating that concerns over competitive pressures are

Trade with 70% Backtested Accuracy

Analyst Views on CART

About CART

About the author

Avis Budget Group Stock Surges 28% After Analyst Upgrade

- Stock Recovery: Avis Budget Group's stock rebounded significantly, ending the week 28% higher after a notable drop on Monday, indicating a marked improvement in investor sentiment and renewed confidence in the company's future performance.

- Analyst Upgrade: Jefferies analyst John Colantuoni upgraded Avis's rating to 'buy', based on an analysis of recent developments in artificial intelligence, suggesting a positive outlook for the company amidst evolving market dynamics.

- Market Dynamics Impact: Despite benefiting from chaos at U.S. airports, analysts warn that surging oil prices are driving up gas prices, which may deter consumers from renting cars, particularly as Avis's fleet consists largely of traditional gas-powered vehicles, posing a significant challenge.

- Changing Competitive Landscape: Colantuoni believes that companies like Avis and Instacart will benefit directly from advancements in AI rather than compete against it, presenting new growth opportunities for Avis, even as it navigates external economic pressures.

Avis Budget Group Stock Surges After Analyst Upgrade

- Analyst Upgrade: Jefferies analyst John Colantuoni upgraded Avis Budget Group to a buy rating, believing the company's potential in artificial intelligence will directly benefit its stock, boosting investor confidence.

- Significant Price Recovery: After a notable drop on Monday, Avis's stock surged 28% by the end of the week, reflecting a positive market sentiment despite concerns over dilution from a secondary share issue.

- Market Environment Challenges: While Avis has benefited from chaos at U.S. airports, rising oil prices are making consumers hesitant to rent cars, particularly since most of its fleet consists of traditional gas-powered vehicles, which could impact future rental demand.

- Investor Caution: Despite the stock's rebound, the Motley Fool analyst team did not include Avis in their current list of top investment stocks, advising investors to carefully consider market dynamics before making decisions.

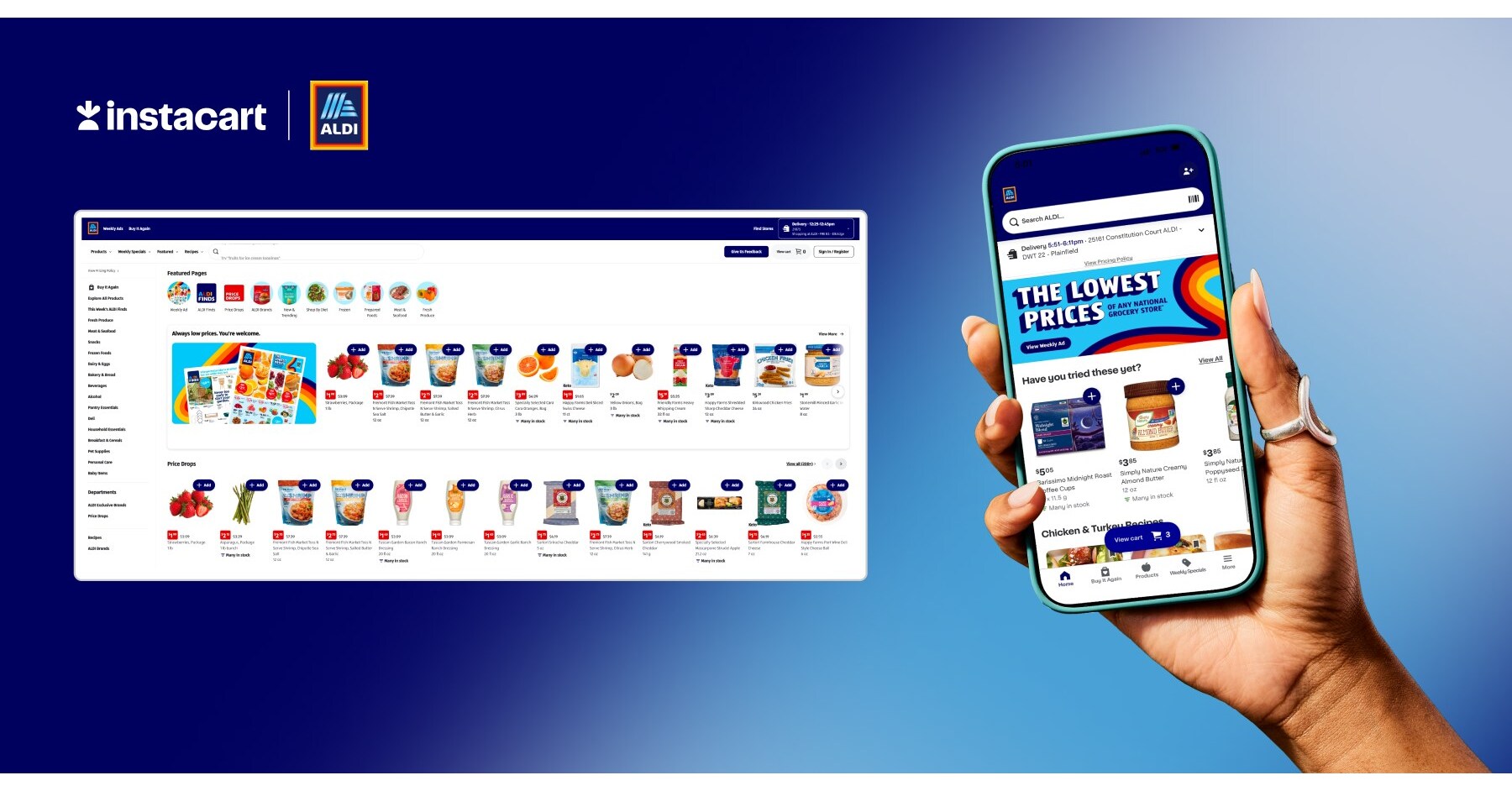

ALDI Partners with Instacart to Enhance Online Shopping Experience

- Partnership Deepening: Instacart's collaboration with ALDI, which began in 2017, has now evolved into an exclusive fulfillment partnership, leveraging the Storefront Pro platform to enhance the online shopping experience and is expected to further drive ALDI's market expansion in the U.S.

- Technology Upgrade: The new website and mobile app provide personalized product recommendations and enhanced product discovery through Instacart's enterprise-grade solutions, allowing customers to enjoy a more convenient shopping experience across ALDI's 2,600+ stores, thereby improving customer satisfaction.

- Rapid Delivery Capability: Since 2019, Instacart's fulfillment solutions have enabled ALDI customers to receive high-quality delivery and curbside pickup in as fast as one hour, ensuring time and cost efficiency for shoppers.

- Market Leadership: According to the 2026 dunnhumby Retailer Preference Index report, ALDI is recognized as the number one in

Instacart Shares Rise 5% Following Jefferies Upgrade to 'Buy'

Stock Performance: Shares of Instacart have increased by 5% following a positive upgrade from Jeffries, which changed its rating to 'Buy'.

Market Reaction: The upgrade reflects a favorable outlook on Instacart's business prospects, influencing investor sentiment and stock valuation.

Analyst Insights: Jeffries' analysts provided insights into the company's potential growth, contributing to the decision to upgrade the stock rating.

Investment Implications: The upgrade may attract more investors to Instacart, potentially leading to further increases in share price and market interest.

Latest Wall Street Rating Updates

- UBS Upgrade: UBS upgrades Adecoagro from Neutral to Buy, raising the price target from $8 to $16.2, indicating the company is poised to benefit from the ongoing Middle East conflict, which is expected to enhance its financial performance.

- HSBC Bullish on Carnival: HSBC upgrades Carnival from Hold to Buy, asserting that the current share price undervalues the resilience of experience-led demand, which is likely to improve the company's market performance in the near future.

- Morgan Stanley Reiterates Meta: Morgan Stanley lowers its price target for Meta from $825 to $775 but maintains it as a top investment idea, suggesting that market sentiment has bottomed out, making it an opportune time to buy.

- Deutsche Bank Upgrades Colgate: Deutsche Bank upgrades Colgate-Palmolive from Hold to Buy, highlighting the company's core business as having long-term investment value and the ability to weather current market volatility effectively.

MAPLEBEAR INC: JEFFERIES UPGRADES TO BUY FROM HOLD; INCREASES TARGET PRICE TO $45 FROM $38

- Company Update: Maple Bear has raised its target price to $45 from $38.

- Investment Strategy: Jeffries is set to buy from Hold, indicating a shift in investment stance.

Avis Budget Group Stock Surges 28% After Analyst Upgrade

- Stock Recovery: Avis Budget Group's stock rebounded significantly, ending the week 28% higher after a notable drop on Monday, indicating a marked improvement in investor sentiment and renewed confidence in the company's future performance.

- Analyst Upgrade: Jefferies analyst John Colantuoni upgraded Avis's rating to 'buy', based on an analysis of recent developments in artificial intelligence, suggesting a positive outlook for the company amidst evolving market dynamics.

- Market Dynamics Impact: Despite benefiting from chaos at U.S. airports, analysts warn that surging oil prices are driving up gas prices, which may deter consumers from renting cars, particularly as Avis's fleet consists largely of traditional gas-powered vehicles, posing a significant challenge.

- Changing Competitive Landscape: Colantuoni believes that companies like Avis and Instacart will benefit directly from advancements in AI rather than compete against it, presenting new growth opportunities for Avis, even as it navigates external economic pressures.

Avis Budget Group Stock Surges After Analyst Upgrade

- Analyst Upgrade: Jefferies analyst John Colantuoni upgraded Avis Budget Group to a buy rating, believing the company's potential in artificial intelligence will directly benefit its stock, boosting investor confidence.

- Significant Price Recovery: After a notable drop on Monday, Avis's stock surged 28% by the end of the week, reflecting a positive market sentiment despite concerns over dilution from a secondary share issue.

- Market Environment Challenges: While Avis has benefited from chaos at U.S. airports, rising oil prices are making consumers hesitant to rent cars, particularly since most of its fleet consists of traditional gas-powered vehicles, which could impact future rental demand.

- Investor Caution: Despite the stock's rebound, the Motley Fool analyst team did not include Avis in their current list of top investment stocks, advising investors to carefully consider market dynamics before making decisions.

ALDI Partners with Instacart to Enhance Online Shopping Experience

- Partnership Deepening: Instacart's collaboration with ALDI, which began in 2017, has now evolved into an exclusive fulfillment partnership, leveraging the Storefront Pro platform to enhance the online shopping experience and is expected to further drive ALDI's market expansion in the U.S.

- Technology Upgrade: The new website and mobile app provide personalized product recommendations and enhanced product discovery through Instacart's enterprise-grade solutions, allowing customers to enjoy a more convenient shopping experience across ALDI's 2,600+ stores, thereby improving customer satisfaction.

- Rapid Delivery Capability: Since 2019, Instacart's fulfillment solutions have enabled ALDI customers to receive high-quality delivery and curbside pickup in as fast as one hour, ensuring time and cost efficiency for shoppers.

- Market Leadership: According to the 2026 dunnhumby Retailer Preference Index report, ALDI is recognized as the number one in

Instacart Shares Rise 5% Following Jefferies Upgrade to 'Buy'

Stock Performance: Shares of Instacart have increased by 5% following a positive upgrade from Jeffries, which changed its rating to 'Buy'.

Market Reaction: The upgrade reflects a favorable outlook on Instacart's business prospects, influencing investor sentiment and stock valuation.

Analyst Insights: Jeffries' analysts provided insights into the company's potential growth, contributing to the decision to upgrade the stock rating.

Investment Implications: The upgrade may attract more investors to Instacart, potentially leading to further increases in share price and market interest.

Latest Wall Street Rating Updates

- UBS Upgrade: UBS upgrades Adecoagro from Neutral to Buy, raising the price target from $8 to $16.2, indicating the company is poised to benefit from the ongoing Middle East conflict, which is expected to enhance its financial performance.

- HSBC Bullish on Carnival: HSBC upgrades Carnival from Hold to Buy, asserting that the current share price undervalues the resilience of experience-led demand, which is likely to improve the company's market performance in the near future.

- Morgan Stanley Reiterates Meta: Morgan Stanley lowers its price target for Meta from $825 to $775 but maintains it as a top investment idea, suggesting that market sentiment has bottomed out, making it an opportune time to buy.

- Deutsche Bank Upgrades Colgate: Deutsche Bank upgrades Colgate-Palmolive from Hold to Buy, highlighting the company's core business as having long-term investment value and the ability to weather current market volatility effectively.

MAPLEBEAR INC: JEFFERIES UPGRADES TO BUY FROM HOLD; INCREASES TARGET PRICE TO $45 FROM $38

- Company Update: Maple Bear has raised its target price to $45 from $38.

- Investment Strategy: Jeffries is set to buy from Hold, indicating a shift in investment stance.