FutureFuel Q4 Revenue $19.84M, Down Year-over-Year

Reports Q4 revenue $19.84M vs. $61.51M last year. "Excluding a $5.6 million LIFO adjustment, our fourth-quarter results demonstrate resilience and steady improvement despite challenging market conditions. While 2025 volumes in our Chemicals and Biofuels segments were pressured by soft demand, regulatory shifts, and high input costs, we utilized this period to fortify our foundations, focusing on operational turnarounds and enhancing plant reliability. In the Chemicals segment, we completed construction of a new methacrylate plant, enabling backward integration into a key raw material and positioning us as a market supplier. The plant became operational late in the fourth quarter and is now fully qualified. We expect meaningful revenue contributions beginning in 2026. We also advanced several growth projects, including customer-backed capacity expansions and a significant production line upgrade, with contributions to revenue and margins anticipated toward the end of 2026. Demand opportunities continue to expand, supported by reshoring trends and our value proposition as a centrally located, efficient custom chemical manufacturer. The Biofuel segment faced significant headwinds in 2025 following the expiration of the blenders tax credit and initial uncertainty surrounding the IRA 45Z replacement. This led to a strategic inventory reduction in the first half of the year and a temporary production pause. However, the release of final 45Z guidance has provided much-needed regulatory clarity through 2029. With Renewable Volume Obligations expected to rise in 2026 and 2027, we have resumed raw material procurement and initiated a gradual restart of production. Looking ahead to 2026, we are increasingly optimistic about the Biodiesel segment, supported by improved regulatory clarity despite continued elevated input costs. While chemical market demand is expected to remain soft, we anticipate higher utilization of our new methacrylate unit and increased production as expansion projects come online. Following weather-related downtime in January, we expect improved operating performance throughout the year. Finally, we will celebrate our 50th anniversary this year. Over five decades, we have supplied critical specialty chemistries to many of the world's leading consumer goods and chemical companies. We value these long-standing partnerships and look forward to continued success in the years ahead." said Roeland Polet, CEO for FutureFuel.

Trade with 70% Backtested Accuracy

Analyst Views on FF

About FF

About the author

First Mining Gold Announces 2026 AGM Voting Results

- Shareholder Voting Overview: At the 2026 AGM, a total of 501,078,315 common shares were represented, accounting for 36.20% of the company's outstanding shares, indicating strong shareholder engagement and enhancing the legitimacy of management decisions.

- Director Election Results: All five director nominees received over 88% support, with Daniel W. Wilton elected at 99.59%, reflecting shareholder trust in the leadership and potentially facilitating the smooth implementation of future strategies.

- Auditor Appointment Approved: The appointment of the auditor was carried with a high approval rate of 98.59%, which not only underscores shareholder emphasis on financial transparency but also provides a stable foundation for future financial audits.

- Project Progress Overview: First Mining is advancing two major gold projects in Canada, Springpole and Duparquet, with the former's Environmental Impact Statement submitted in 2024, demonstrating proactive resource development that may lay the groundwork for future revenue growth.

On-Demand Access to Precious Metals & Critical Minerals Virtual Investor Conference Presentations

- Conference Content Replay: Presentations from the Precious Metals & Critical Minerals Virtual Investor Conference are now available for on-demand viewing, allowing investors, advisors, and analysts to access content 24/7 for 90 days, thereby enhancing convenience and flexibility in information retrieval.

- One-on-One Meeting Arrangements: Selected companies are accepting requests for one-on-one management meetings, enabling investors to communicate directly with company leadership, which enhances interaction and transparency between investors and companies.

- Resource Download Convenience: Attendees can download investor materials from the company's resource section, which not only provides comprehensive information support for investors but also promotes a deeper understanding of the company's business.

- Advantages of Virtual Conferences: Virtual Investor Conferences offer real-time investor engagement solutions that improve the efficiency of connections between companies and investors, marking a new trend in investor relations management, especially among retail and institutional investors globally.

Precious Metals & Critical Minerals Virtual Investor Conference Announced

- Conference Agenda Released: The Precious Metals & Critical Minerals Virtual Investor Conference is set for May 5-7, 2026, attracting individual and institutional investors, which is expected to enhance market attention on the sector due to strong investor interest.

- Ease of Participation: Investors can register for free and attend the conference, with system checks designed to expedite participation and ensure timely updates, thereby increasing engagement and interaction during the event.

- Diverse Company Presentations: The conference will feature multiple companies, including Novo Resources Corp. and Atlas Lithium Corp., providing investors with a wealth of investment opportunities that could further drive capital inflow into the precious metals and critical minerals sectors.

- Enhanced Investor Interaction: The virtual format offers a real-time interactive platform for companies to hold one-on-one meetings with investors, improving the efficiency of investor relations management and facilitating direct communication between companies and potential investors.

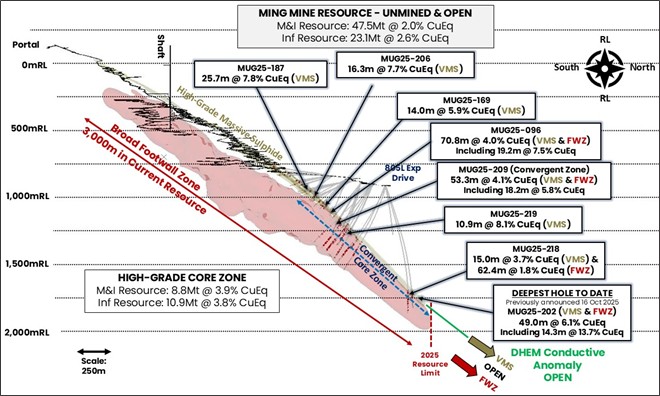

FireFly Metals Reports Significant Progress at Green Bay Copper-Gold Project

- High-Grade Core Zone Results: Recent drilling at the Green Bay Copper-Gold Project revealed results of 70.8m @ 4.0% CuEq and 53.3m @ 4.1% CuEq, further confirming the scale and continuity of the high-grade core zone, which is expected to positively impact future production economics.

- Mineral Resource Estimate Update: The current mineral resource estimate stands at 50.4Mt @ 2.0% CuEq, with an update planned for June 2026 to support the Preliminary Economic Assessment (PEA), providing crucial insights into the project's feasibility.

- Strategic Transaction Completion: FireFly successfully completed the sale of its Ontario gold assets to Bellavista Resources, which is expected to create value for shareholders through the distribution of Bellavista shares, with the transaction finalized on April 29, 2026.

- Strong Funding and Future Plans: As of March 31, 2026, FireFly reported approximately A$219.9 million in cash and liquid investments, sufficient to support its growth drilling program and economic studies, accelerating the path to resuming copper-gold production.

FutureFuel to Release Q1 2026 Financial Results on May 11

- Earnings Release Schedule: FutureFuel will announce its financial results for the first quarter ending March 31, 2026, after market close on May 11, 2026, with details available on the company's website, ensuring transparency and timely communication with investors.

- Company Overview: FutureFuel is a leading manufacturer of custom and performance chemicals and biofuels, with its chemicals segment focusing on providing custom chemicals for specific customers and multi-customer specialty chemicals, showcasing its diversified capabilities in the chemical industry.

- Diverse Product Portfolio: FutureFuel's custom manufacturing product portfolio includes proprietary agrochemicals, adhesion promoters, a biocide intermediate, and an antioxidant precursor, demonstrating its ability to respond flexibly to specific market demands.

- Biofuel Production: The company's biofuels segment primarily produces and sells biodiesel, catering to customer demand for renewable energy, reflecting its strategic positioning in the sustainable development sector.

Gold Exploration Budgets Surge Amid Production Declines

- Surge in Exploration Budgets: Global gold exploration budgets reached $6.2 billion in 2025, marking an 11% increase and accounting for 50% of all exploration spending, highlighting the pressure on major miners facing production declines due to depleting reserves.

- Emergence of Junior Companies: With major miners under pressure, five junior companies are conducting early-stage discovery work in underexplored areas, positioning themselves strategically within the supply chain to capitalize on the growing demand for gold.

- Gran Esperanza Project Progress: Golden Goose Resources has initiated the first phase of fieldwork at its Gran Esperanza gold-silver project in Argentina, aiming to establish the strength and consistency of gold and silver grades through systematic sampling and geological mapping, setting the stage for future drilling.

- Strategic Importance of Drilling Plans: Companies like First Mining Gold and GoldMining are actively advancing drilling programs, with First Mining reporting significant results from its Duparquet project and GoldMining launching an 8,000-meter drill campaign at its São Jorge project in Brazil, underscoring the market's strong demand for gold resources.

First Mining Gold Announces 2026 AGM Voting Results

- Shareholder Voting Overview: At the 2026 AGM, a total of 501,078,315 common shares were represented, accounting for 36.20% of the company's outstanding shares, indicating strong shareholder engagement and enhancing the legitimacy of management decisions.

- Director Election Results: All five director nominees received over 88% support, with Daniel W. Wilton elected at 99.59%, reflecting shareholder trust in the leadership and potentially facilitating the smooth implementation of future strategies.

- Auditor Appointment Approved: The appointment of the auditor was carried with a high approval rate of 98.59%, which not only underscores shareholder emphasis on financial transparency but also provides a stable foundation for future financial audits.

- Project Progress Overview: First Mining is advancing two major gold projects in Canada, Springpole and Duparquet, with the former's Environmental Impact Statement submitted in 2024, demonstrating proactive resource development that may lay the groundwork for future revenue growth.

On-Demand Access to Precious Metals & Critical Minerals Virtual Investor Conference Presentations

- Conference Content Replay: Presentations from the Precious Metals & Critical Minerals Virtual Investor Conference are now available for on-demand viewing, allowing investors, advisors, and analysts to access content 24/7 for 90 days, thereby enhancing convenience and flexibility in information retrieval.

- One-on-One Meeting Arrangements: Selected companies are accepting requests for one-on-one management meetings, enabling investors to communicate directly with company leadership, which enhances interaction and transparency between investors and companies.

- Resource Download Convenience: Attendees can download investor materials from the company's resource section, which not only provides comprehensive information support for investors but also promotes a deeper understanding of the company's business.

- Advantages of Virtual Conferences: Virtual Investor Conferences offer real-time investor engagement solutions that improve the efficiency of connections between companies and investors, marking a new trend in investor relations management, especially among retail and institutional investors globally.

Precious Metals & Critical Minerals Virtual Investor Conference Announced

- Conference Agenda Released: The Precious Metals & Critical Minerals Virtual Investor Conference is set for May 5-7, 2026, attracting individual and institutional investors, which is expected to enhance market attention on the sector due to strong investor interest.

- Ease of Participation: Investors can register for free and attend the conference, with system checks designed to expedite participation and ensure timely updates, thereby increasing engagement and interaction during the event.

- Diverse Company Presentations: The conference will feature multiple companies, including Novo Resources Corp. and Atlas Lithium Corp., providing investors with a wealth of investment opportunities that could further drive capital inflow into the precious metals and critical minerals sectors.

- Enhanced Investor Interaction: The virtual format offers a real-time interactive platform for companies to hold one-on-one meetings with investors, improving the efficiency of investor relations management and facilitating direct communication between companies and potential investors.

FireFly Metals Reports Significant Progress at Green Bay Copper-Gold Project

- High-Grade Core Zone Results: Recent drilling at the Green Bay Copper-Gold Project revealed results of 70.8m @ 4.0% CuEq and 53.3m @ 4.1% CuEq, further confirming the scale and continuity of the high-grade core zone, which is expected to positively impact future production economics.

- Mineral Resource Estimate Update: The current mineral resource estimate stands at 50.4Mt @ 2.0% CuEq, with an update planned for June 2026 to support the Preliminary Economic Assessment (PEA), providing crucial insights into the project's feasibility.

- Strategic Transaction Completion: FireFly successfully completed the sale of its Ontario gold assets to Bellavista Resources, which is expected to create value for shareholders through the distribution of Bellavista shares, with the transaction finalized on April 29, 2026.

- Strong Funding and Future Plans: As of March 31, 2026, FireFly reported approximately A$219.9 million in cash and liquid investments, sufficient to support its growth drilling program and economic studies, accelerating the path to resuming copper-gold production.

FutureFuel to Release Q1 2026 Financial Results on May 11

- Earnings Release Schedule: FutureFuel will announce its financial results for the first quarter ending March 31, 2026, after market close on May 11, 2026, with details available on the company's website, ensuring transparency and timely communication with investors.

- Company Overview: FutureFuel is a leading manufacturer of custom and performance chemicals and biofuels, with its chemicals segment focusing on providing custom chemicals for specific customers and multi-customer specialty chemicals, showcasing its diversified capabilities in the chemical industry.

- Diverse Product Portfolio: FutureFuel's custom manufacturing product portfolio includes proprietary agrochemicals, adhesion promoters, a biocide intermediate, and an antioxidant precursor, demonstrating its ability to respond flexibly to specific market demands.

- Biofuel Production: The company's biofuels segment primarily produces and sells biodiesel, catering to customer demand for renewable energy, reflecting its strategic positioning in the sustainable development sector.

Gold Exploration Budgets Surge Amid Production Declines

- Surge in Exploration Budgets: Global gold exploration budgets reached $6.2 billion in 2025, marking an 11% increase and accounting for 50% of all exploration spending, highlighting the pressure on major miners facing production declines due to depleting reserves.

- Emergence of Junior Companies: With major miners under pressure, five junior companies are conducting early-stage discovery work in underexplored areas, positioning themselves strategically within the supply chain to capitalize on the growing demand for gold.

- Gran Esperanza Project Progress: Golden Goose Resources has initiated the first phase of fieldwork at its Gran Esperanza gold-silver project in Argentina, aiming to establish the strength and consistency of gold and silver grades through systematic sampling and geological mapping, setting the stage for future drilling.

- Strategic Importance of Drilling Plans: Companies like First Mining Gold and GoldMining are actively advancing drilling programs, with First Mining reporting significant results from its Duparquet project and GoldMining launching an 8,000-meter drill campaign at its São Jorge project in Brazil, underscoring the market's strong demand for gold resources.