Atlas Energy's Pivot: New Opportunities in Natural Gas Power Generation

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Mar 23 2026

0mins

Source: NASDAQ.COM

- Strategic Transformation: Atlas Energy is pivoting by leveraging stranded Permian natural gas, aiming to build up to 2 gigawatts of generation capacity by 2030, which is expected to significantly reshape its long-term earnings profile and transition the company into a contracted infrastructure business.

- Market Demand: With hyperscalers projected to invest $690 billion in AI infrastructure by 2026, the urgent need for power sources is driving Atlas Energy to accelerate its power business development to meet the increasing electricity demands.

- Partnership Agreement: Atlas has signed a Global Framework Agreement with Caterpillar, securing approximately 1.4 gigawatts of natural gas power generation assets by 2030, with an initial purchase commitment of about $840 million, laying the groundwork for successful deployment of its power business.

- Business Diversification: Atlas's business model consists of three pillars: proppant sales, logistics (Dune Express), and Power-as-a-Service, with the introduction of the power segment transforming its cyclical commodity business into a more stable contracted infrastructure play, despite facing profitability pressures in the short term.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy AESI?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on AESI

Wall Street analysts forecast AESI stock price to fall

9 Analyst Rating

2 Buy

4 Hold

3 Sell

Hold

Current: 17.020

Low

7.00

Averages

10.49

High

16.00

Current: 17.020

Low

7.00

Averages

10.49

High

16.00

About AESI

Atlas Energy Solutions Inc. is a solution provider to the energy industry. Its portfolio of offerings includes oilfield logistics, distributed power systems, and the proppant supply network in the Permian Basin. Its hundred percent of Atlas LLC’s sand reserves are located in Texas within the Permian Basin and operations consist of proppant production and processing facilities, including four facilities near Kermit, Texas (together, the Kermit facilities), a fifth facility near Monahans, Texas, and the OnCore distributed mining network. The sand and logistics segments provide locally sourced over 100 mesh and 40/70 sand used as a proppant during the well completion process. Also, it provides a differentiated logistics platform that includes its fleet of fit-for-purpose trucks, trailers, and the Dune Express, an overland conveyor infrastructure solution. The Power segment provides distributed power solutions through a fleet of more than 1,000 natural gas-powered reciprocating generators.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

SPDR S&P Oil & Gas ETF Underperforms

- ETF Performance: The SPDR S&P Oil & Gas Equipment & Services ETF is down approximately 1.8% in Thursday afternoon trading, indicating market concerns about the sector that could impact investor confidence.

- Weak Individual Stocks: Within the ETF, Atlas Energy Solutions shares fell about 6%, while Flowco Holdings dropped approximately 4.7%, reflecting poor market performance for these companies that may lead investors to reassess their portfolios.

- Market Sentiment Impact: The overall weak performance of the oil and gas sector may cause investors to adopt a cautious stance towards related stocks, potentially affecting capital inflows into the industry.

- Uncertain Industry Outlook: Given the current economic environment, the oil and gas equipment and services sector faces challenges that could suppress the ETF's long-term performance, prompting investors to monitor industry developments for informed decision-making.

See More

ATLAS ENERGY SOLUTIONS: BARCLAYS INCREASES TARGET PRICE FROM $12 TO $16

Barclays Raises Price Target: Barclays has increased its price target for Atlas Energy Solutions to $16 from a previous target of $12.

Market Implications: This adjustment reflects Barclays' positive outlook on Atlas Energy Solutions and may influence investor sentiment and market performance.

See More

Atlas Energy (AESI) Q1 2026 Earnings Transcript

See More

Atlas Energy Q1 Earnings: Revenue Beats Expectations

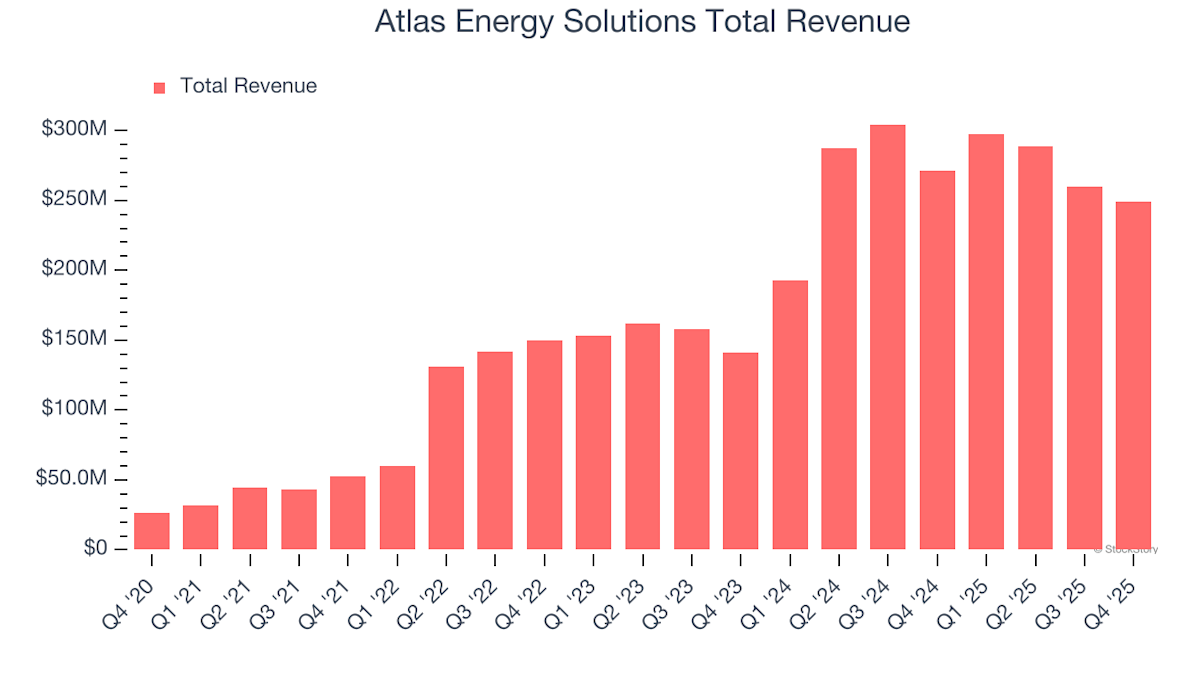

- Earnings Performance: Atlas Energy Solutions reported a Q1 GAAP EPS of -$0.38, missing expectations by $0.12, indicating challenges in profitability, although revenue of $265.5 million, down 10.8% year-over-year, exceeded expectations by $9.39 million, reflecting market demand fluctuations.

- Rising Expenses: Selling, general, and administrative expenses increased by $2 million in Q1 compared to Q4 2025, reaching $35.7 million or 5.9% of total revenue, indicating pressure on the company’s cost control, which may impact future profitability.

- Liquidity Position: As of March 31, 2026, the company’s total liquidity stood at $89.5 million, comprising $39.8 million in cash and cash equivalents and $49.7 million available under the 2023 ABL Credit Facility, demonstrating relative stability in cash management but necessitating attention to future capital expenditures.

- Future Guidance: The company provided financial guidance for Q2 2026, based on current market outlook and plans, but due to various known and unknown uncertainties, actual results may differ materially from the guidance, reflecting the complexities of the market environment.

See More

ATLAS ENERGY SOLUTIONS REPORTS Q1 SALES OF USD 265.583 MILLION, BEATING IBES ESTIMATE OF USD 258.3 MILLION

- Sales Performance: Atlas Energy Solutions reported Q1 sales of USD 265.58 million.

- Comparison with Estimates: This figure exceeds the Ibes estimate of USD 258.3 million.

See More

Atlas Energy Solutions Earnings Preview

- Earnings Expectations: Atlas Energy Solutions is set to report earnings after the bell on Monday, with market expectations indicating a 13.8% year-over-year revenue decline, contrasting sharply with last year's 54.5% growth, highlighting increased industry volatility.

- Last Quarter Performance: The company reported revenues of $249.4 million last quarter, down 8.1% year-over-year, yet it exceeded analysts' EBITDA estimates, indicating resilience in profitability amidst challenges.

- Market Sentiment: Investor sentiment in the oilfield services sector has been positive, with average share prices rising 4.1% over the past month, while Atlas Energy Solutions saw a remarkable 55.4% increase during the same period, reflecting strong market confidence in its future performance.

- Analyst Outlook: Despite missing Wall Street's revenue estimates multiple times over the past two years, most analysts have reaffirmed their expectations in the last 30 days, with an average price target of $15.36 compared to the current share price of $17.34, suggesting optimism about its future.

See More

SPDR S&P Oil & Gas ETF Underperforms

- ETF Performance: The SPDR S&P Oil & Gas Equipment & Services ETF is down approximately 1.8% in Thursday afternoon trading, indicating market concerns about the sector that could impact investor confidence.

- Weak Individual Stocks: Within the ETF, Atlas Energy Solutions shares fell about 6%, while Flowco Holdings dropped approximately 4.7%, reflecting poor market performance for these companies that may lead investors to reassess their portfolios.

- Market Sentiment Impact: The overall weak performance of the oil and gas sector may cause investors to adopt a cautious stance towards related stocks, potentially affecting capital inflows into the industry.

- Uncertain Industry Outlook: Given the current economic environment, the oil and gas equipment and services sector faces challenges that could suppress the ETF's long-term performance, prompting investors to monitor industry developments for informed decision-making.

See More

ATLAS ENERGY SOLUTIONS: BARCLAYS INCREASES TARGET PRICE FROM $12 TO $16

Barclays Raises Price Target: Barclays has increased its price target for Atlas Energy Solutions to $16 from a previous target of $12.

Market Implications: This adjustment reflects Barclays' positive outlook on Atlas Energy Solutions and may influence investor sentiment and market performance.

See More

Atlas Energy (AESI) Q1 2026 Earnings Transcript

See More

Atlas Energy Q1 Earnings: Revenue Beats Expectations

- Earnings Performance: Atlas Energy Solutions reported a Q1 GAAP EPS of -$0.38, missing expectations by $0.12, indicating challenges in profitability, although revenue of $265.5 million, down 10.8% year-over-year, exceeded expectations by $9.39 million, reflecting market demand fluctuations.

- Rising Expenses: Selling, general, and administrative expenses increased by $2 million in Q1 compared to Q4 2025, reaching $35.7 million or 5.9% of total revenue, indicating pressure on the company’s cost control, which may impact future profitability.

- Liquidity Position: As of March 31, 2026, the company’s total liquidity stood at $89.5 million, comprising $39.8 million in cash and cash equivalents and $49.7 million available under the 2023 ABL Credit Facility, demonstrating relative stability in cash management but necessitating attention to future capital expenditures.

- Future Guidance: The company provided financial guidance for Q2 2026, based on current market outlook and plans, but due to various known and unknown uncertainties, actual results may differ materially from the guidance, reflecting the complexities of the market environment.

See More

ATLAS ENERGY SOLUTIONS REPORTS Q1 SALES OF USD 265.583 MILLION, BEATING IBES ESTIMATE OF USD 258.3 MILLION

- Sales Performance: Atlas Energy Solutions reported Q1 sales of USD 265.58 million.

- Comparison with Estimates: This figure exceeds the Ibes estimate of USD 258.3 million.

See More

Atlas Energy Solutions Earnings Preview

- Earnings Expectations: Atlas Energy Solutions is set to report earnings after the bell on Monday, with market expectations indicating a 13.8% year-over-year revenue decline, contrasting sharply with last year's 54.5% growth, highlighting increased industry volatility.

- Last Quarter Performance: The company reported revenues of $249.4 million last quarter, down 8.1% year-over-year, yet it exceeded analysts' EBITDA estimates, indicating resilience in profitability amidst challenges.

- Market Sentiment: Investor sentiment in the oilfield services sector has been positive, with average share prices rising 4.1% over the past month, while Atlas Energy Solutions saw a remarkable 55.4% increase during the same period, reflecting strong market confidence in its future performance.

- Analyst Outlook: Despite missing Wall Street's revenue estimates multiple times over the past two years, most analysts have reaffirmed their expectations in the last 30 days, with an average price target of $15.36 compared to the current share price of $17.34, suggesting optimism about its future.

See More