Corpay, Inc. Reports Strong Q4 2025 Earnings Exceeding Expectations

- Significant Revenue Growth: Corpay reported Q4 2025 revenue of $1.248 billion, a 21% year-over-year increase that exceeded expectations, primarily driven by strong performance in cross-border payments and the Alpha business, indicating sustained competitive strength in the market.

- Record EPS Achievement: The adjusted EPS for Q4 reached $6.04, up 13% year-over-year, while the full-year EPS was $21.38, reflecting a 12% growth, which underscores the company's improving profitability and enhances investor confidence.

- Optimistic 2026 Outlook: The company projects 2026 revenue to hit $5.265 billion, a 16% increase, with EPS guidance set at $26, growing 22%, demonstrating management's strong confidence in future growth, particularly in corporate payments and acquisition integration.

- Strategic Investments and Portfolio Simplification: Management emphasized ongoing portfolio simplification and strategic investments, planning to divest the vehicle payments business while reallocating resources to enhance corporate payments, aiming to adapt to market changes and improve overall operational efficiency.

Trade with 70% Backtested Accuracy

Analyst Views on CPAY

About CPAY

About the author

TA Connections Expands Passenger Support Services for Aircalin

- Service Expansion: TA Connections has extended its partnership with Aircalin, enhancing passenger support services across a broader international network, including major airports like Paris Charles de Gaulle and Singapore Changi, thereby improving service coverage and responsiveness.

- New Destinations Added: The expanded service now includes key international destinations such as Paris, Sydney, and Singapore, with full implementation expected in the coming months, which will further bolster Aircalin's global service capabilities.

- Operational Efficiency Improvement: Through TA Connections' services, Aircalin will benefit from faster access to hotel inventory, globally negotiated hotel rates, and comprehensive invoice reconciliation, which will reduce administrative burdens and enhance operational responsiveness.

- Customer Experience Optimization: The services provided by TA Connections are designed to help airlines streamline disruption logistics, control costs, and deliver a consistent, high-quality experience for passengers when it matters most, thereby enhancing Aircalin's competitive position in the market.

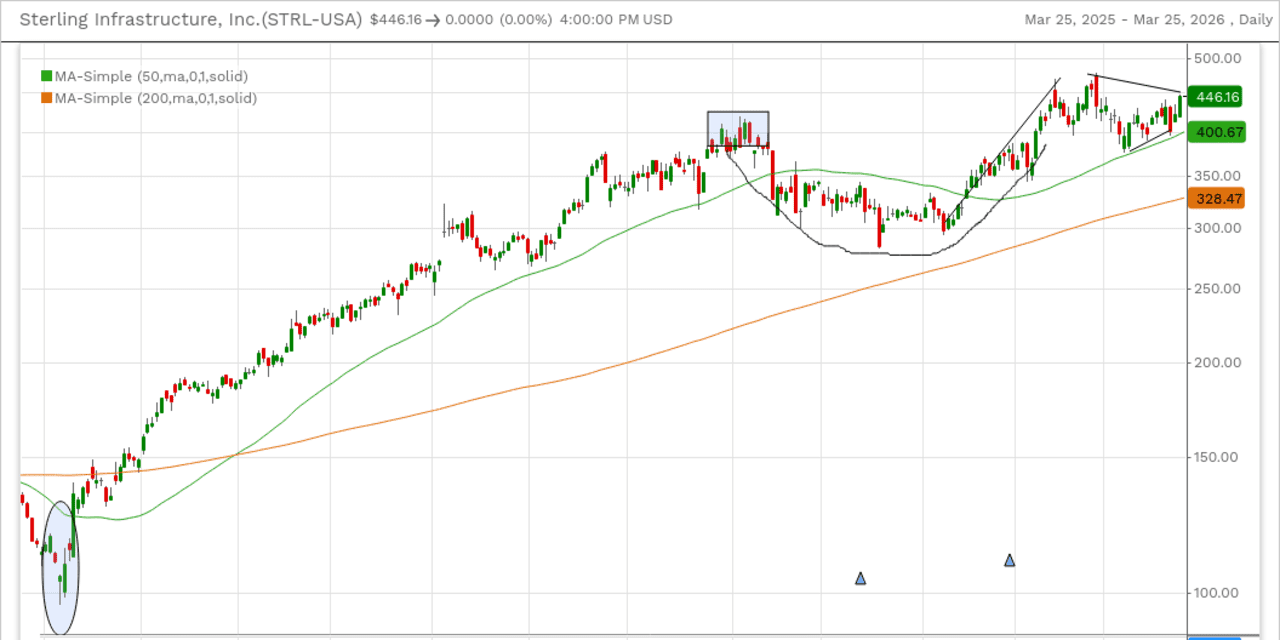

A Look Back at Previous Stock Selections: Sterling Infrastructure, Corpay, Deere

Importance of Revisiting Stock Picks: Reviewing former stock picks helps investors measure effectiveness and refine their strategies and discipline.

Identifying Patterns and Assumptions: By analyzing past calls, investors can recognize successful patterns and identify incorrect assumptions that may have influenced decisions.

Improving Decision-Making: Regular evaluations of past investments enhance future decision-making processes by learning from previous outcomes.

Reinforcing Accountability: This practice ensures that investment ideas are assessed based on their market performance, not just the initial investment thesis.

Corpay to Host Virtual Teach-In on Cross-Border Business

- Event Announcement: Corpay will host a virtual teach-in on its Cross-Border Business on May 13, 2026, which is expected to attract global clients and enhance the company's visibility and influence in the cross-border payments sector.

- Executive Participation: CEO Ron Clarke, CFO Peter Walker, and Cross-Border Group President Mark Frey will co-host the event, showcasing the management's commitment to the cross-border business and its strategic direction.

- In-Depth Content: The management team will discuss the company's cross-border franchises, competitive position, and growth drivers, aiming to bolster investor confidence in the company's future and enhance shareholder value.

- Information Dissemination: Detailed information and presentation materials will be published on Corpay's Investor Relations website in advance, ensuring investors can access timely information, thereby increasing transparency and trust.

US-Iran Tensions Ease, Boosting Stock Market Rally

- Market Rally: President Trump announced ongoing negotiations to ease hostilities with Iran, resulting in a significant stock market surge, with major indices like the S&P 500 and Dow sharply rising, creating a 'risk-on' environment favorable to financial firms.

- Asset Management Gains: The rise in equity values boosts the assets under management (AUM) for asset management firms, a key performance metric, as seen with Evercore (EVR) jumping 3.2%, highlighting the positive impact on the investment banking sector.

- Energy Price Drop: The easing of tensions led to a more than 7% drop in Brent crude oil prices, which not only affects the energy sector but also potentially lowers costs for consumers, further enhancing market sentiment.

- Payoneer Volatility: Payoneer (PAYO) shares rose 7.5%, despite an 11.7% decline year-to-date, indicating that today's market movement is significant, although it may not fundamentally alter perceptions of the company's business outlook.

Corpay Becomes Exclusive FX Provider for Formula E

- Partnership Formation: Corpay, Inc. has announced a partnership with Formula E, the world's first all-electric FIA World Championship, becoming its exclusive foreign exchange provider, marking a strategic expansion into the high-end sports market.

- FX Risk Management: Through this partnership, Corpay will provide comprehensive FX risk management and international payment solutions to support Formula E's global operations across major cities, enhancing its competitiveness in a dynamic multi-currency environment.

- Technology and Sustainability: As the world's first all-electric racing series, Formula E is committed to technological innovation and sustainability, and Corpay's collaboration will further enhance the efficiency of its global financial operations, ensuring smooth operations in a multi-currency environment.

- Market Influence Enhancement: With 150 races successfully held, Formula E attracts participation from renowned automotive manufacturers like Porsche and Jaguar, and Corpay's involvement will strengthen its influence in electric vehicle technology innovation, aiding the transformation of future urban mobility.

Long Path Partners Increases Stake in Alkami Technology

- Share Increase: Long Path Partners LP disclosed a purchase of 572,292 shares of Alkami Technology in Q4 2025, bringing its total stake to $72.5 million, an increase of $8.6 million from the previous quarter, indicating strong confidence in the company's long-term value.

- Portfolio Concentration: Following this purchase, Alkami accounted for approximately 25% of Long Path's assets under management, highlighting the fund's focus on Alkami, which is one of only seven U.S.-listed stocks in its concentrated portfolio.

- Market Performance Analysis: As of February 13, 2026, Alkami's stock traded at $16.27, down 50.4% over the past year and underperforming the S&P 500 by 62.2 percentage points, reflecting market concerns over its short-term volatility.

- Long-Term Growth Potential: Despite short-term challenges, Alkami's revenue grew by 33% in 2025, and the company is gaining traction in sales of its AI-powered solutions, indicating significant long-term growth potential in the digital banking transformation.

TA Connections Expands Passenger Support Services for Aircalin

- Service Expansion: TA Connections has extended its partnership with Aircalin, enhancing passenger support services across a broader international network, including major airports like Paris Charles de Gaulle and Singapore Changi, thereby improving service coverage and responsiveness.

- New Destinations Added: The expanded service now includes key international destinations such as Paris, Sydney, and Singapore, with full implementation expected in the coming months, which will further bolster Aircalin's global service capabilities.

- Operational Efficiency Improvement: Through TA Connections' services, Aircalin will benefit from faster access to hotel inventory, globally negotiated hotel rates, and comprehensive invoice reconciliation, which will reduce administrative burdens and enhance operational responsiveness.

- Customer Experience Optimization: The services provided by TA Connections are designed to help airlines streamline disruption logistics, control costs, and deliver a consistent, high-quality experience for passengers when it matters most, thereby enhancing Aircalin's competitive position in the market.

A Look Back at Previous Stock Selections: Sterling Infrastructure, Corpay, Deere

Importance of Revisiting Stock Picks: Reviewing former stock picks helps investors measure effectiveness and refine their strategies and discipline.

Identifying Patterns and Assumptions: By analyzing past calls, investors can recognize successful patterns and identify incorrect assumptions that may have influenced decisions.

Improving Decision-Making: Regular evaluations of past investments enhance future decision-making processes by learning from previous outcomes.

Reinforcing Accountability: This practice ensures that investment ideas are assessed based on their market performance, not just the initial investment thesis.

Corpay to Host Virtual Teach-In on Cross-Border Business

- Event Announcement: Corpay will host a virtual teach-in on its Cross-Border Business on May 13, 2026, which is expected to attract global clients and enhance the company's visibility and influence in the cross-border payments sector.

- Executive Participation: CEO Ron Clarke, CFO Peter Walker, and Cross-Border Group President Mark Frey will co-host the event, showcasing the management's commitment to the cross-border business and its strategic direction.

- In-Depth Content: The management team will discuss the company's cross-border franchises, competitive position, and growth drivers, aiming to bolster investor confidence in the company's future and enhance shareholder value.

- Information Dissemination: Detailed information and presentation materials will be published on Corpay's Investor Relations website in advance, ensuring investors can access timely information, thereby increasing transparency and trust.

US-Iran Tensions Ease, Boosting Stock Market Rally

- Market Rally: President Trump announced ongoing negotiations to ease hostilities with Iran, resulting in a significant stock market surge, with major indices like the S&P 500 and Dow sharply rising, creating a 'risk-on' environment favorable to financial firms.

- Asset Management Gains: The rise in equity values boosts the assets under management (AUM) for asset management firms, a key performance metric, as seen with Evercore (EVR) jumping 3.2%, highlighting the positive impact on the investment banking sector.

- Energy Price Drop: The easing of tensions led to a more than 7% drop in Brent crude oil prices, which not only affects the energy sector but also potentially lowers costs for consumers, further enhancing market sentiment.

- Payoneer Volatility: Payoneer (PAYO) shares rose 7.5%, despite an 11.7% decline year-to-date, indicating that today's market movement is significant, although it may not fundamentally alter perceptions of the company's business outlook.

Corpay Becomes Exclusive FX Provider for Formula E

- Partnership Formation: Corpay, Inc. has announced a partnership with Formula E, the world's first all-electric FIA World Championship, becoming its exclusive foreign exchange provider, marking a strategic expansion into the high-end sports market.

- FX Risk Management: Through this partnership, Corpay will provide comprehensive FX risk management and international payment solutions to support Formula E's global operations across major cities, enhancing its competitiveness in a dynamic multi-currency environment.

- Technology and Sustainability: As the world's first all-electric racing series, Formula E is committed to technological innovation and sustainability, and Corpay's collaboration will further enhance the efficiency of its global financial operations, ensuring smooth operations in a multi-currency environment.

- Market Influence Enhancement: With 150 races successfully held, Formula E attracts participation from renowned automotive manufacturers like Porsche and Jaguar, and Corpay's involvement will strengthen its influence in electric vehicle technology innovation, aiding the transformation of future urban mobility.

Long Path Partners Increases Stake in Alkami Technology

- Share Increase: Long Path Partners LP disclosed a purchase of 572,292 shares of Alkami Technology in Q4 2025, bringing its total stake to $72.5 million, an increase of $8.6 million from the previous quarter, indicating strong confidence in the company's long-term value.

- Portfolio Concentration: Following this purchase, Alkami accounted for approximately 25% of Long Path's assets under management, highlighting the fund's focus on Alkami, which is one of only seven U.S.-listed stocks in its concentrated portfolio.

- Market Performance Analysis: As of February 13, 2026, Alkami's stock traded at $16.27, down 50.4% over the past year and underperforming the S&P 500 by 62.2 percentage points, reflecting market concerns over its short-term volatility.

- Long-Term Growth Potential: Despite short-term challenges, Alkami's revenue grew by 33% in 2025, and the company is gaining traction in sales of its AI-powered solutions, indicating significant long-term growth potential in the digital banking transformation.