China's Cloud Infrastructure Market Continues Growth

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Feb 10 2026

0mins

Should l Buy TTGT?

Source: Newsfilter

- Market Growth: According to Omdia, Mainland China's cloud infrastructure services market reached $13.4 billion in Q3 2025, growing 24% year-on-year, marking the second consecutive quarter of over 20% growth, indicating sustained enterprise demand and investment in cloud services.

- AI-Driven Market Changes: As enterprises transition from early-stage AI experimentation to broader adoption, AI increasingly drives demand for core cloud infrastructure services, including compute, storage, and databases, accelerating the shift in cloud resource consumption toward production workloads.

- Leading Cloud Providers' Performance: In Q3 2025, Alibaba Cloud, Huawei Cloud, and Tencent Cloud held market shares of 36%, 16%, and 9%, respectively, with Alibaba Cloud achieving triple-digit growth in AI-related revenues for nine consecutive quarters, showcasing its market leadership and strong enterprise collaboration capabilities.

- Technological Innovation and Collaboration: Alibaba Cloud launched nine Qwen3-VL multimodal models, enhancing video understanding and spatial perception, while Huawei Cloud co-launched industry models with China Southern Airlines, reflecting ongoing efforts by cloud providers to innovate and meet the growing market demand for AI applications.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy TTGT?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on TTGT

Wall Street analysts forecast TTGT stock price to rise

3 Analyst Rating

3 Buy

0 Hold

0 Sell

Strong Buy

Current: 5.240

Low

10.00

Averages

11.67

High

15.00

Current: 5.240

Low

10.00

Averages

11.67

High

15.00

About TTGT

TechTarget, Inc., which also refers to itself as Informa TechTarget, is a business-to-business (B2B) growth accelerator that informs, influences and connects the world’s technology buyers and sellers, helping accelerate growth from R&D to return on investment (ROI). It has scale in permissioned B2B first-party data and a unique end-to-end portfolio of data-driven solutions that services the full B2B product lifecycle, from R&D to ROI: from strategy, messaging and content development to in-market activation via brand, demand generation, purchase intent data and sales enablement. In intelligence and advisory, it offers expert analyst, data-driven intelligence products and advisory services to product managers, corporate strategists and the C-suite, challenging market strategies and sharpening product roadmaps. In brand and content, it provides expert editorial, data-driven brand products and content marketing services for brand marketers, product marketers and content marketers.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

China's Cloud Infrastructure Market Continues Growth

- Market Growth: In Q4 2025, China's cloud infrastructure services spending reached $14.7 billion, marking a 26% year-on-year increase, indicating strong market recovery, with a forecasted growth rate of 26% for 2026, reflecting rising enterprise demand for cloud services.

- AI as Growth Driver: AI demand remains the primary growth driver, supporting not only model usage but also broader enterprise AI deployments, alongside rising demand for traditional cloud resources like compute, storage, and databases, indicating a shift in AI's role to a broader infrastructure demand driver.

- Key Vendor Developments: Alibaba Cloud maintained a 37% market share, launching products like Qwen3.5 and Wukong, achieving triple-digit year-on-year growth in AI-related revenue for ten consecutive quarters; Huawei Cloud and Tencent Cloud are also actively advancing their AI strategies to enhance market competitiveness.

- Ecosystem Collaboration: In Q4 2025, partner-driven cloud revenue accounted for 25% of the market, with expectations for further increases, highlighting the importance of ecosystem collaboration in the commercialization of AI, helping enterprises realize business value from AI adoption.

See More

Omdia Forecasts 62.7% Growth in Semiconductor Revenue by 2026

- Market Growth Forecast: Omdia projects a 62.7% increase in semiconductor revenue by 2026, driven primarily by rising memory chip prices and robust demand from AI and data center markets, with computing and data storage revenues expected to rise 90% year-over-year to over $700 billion.

- Memory Chip Demand: Demand for DRAM and NAND chips is anticipated to remain elevated, with the DRAM market nearly doubling in value by 2026 and the NAND segment potentially quadrupling from 2025 levels, highlighting the critical role of memory chips in AI servers.

- Supply Chain Challenges: Despite strong demand, conventional memory supplies remain constrained as manufacturers focus on producing higher-margin High Bandwidth Memory (HBM), with significant supply relief unlikely until 2027, impacting overall market dynamics.

- Risk Factors: Omdia notes that risks to the outlook include tariffs, energy costs, geopolitical tensions, and long-term returns on heavy AI infrastructure spending, which could negatively affect growth in the semiconductor industry.

See More

Omdia Significantly Raises Semiconductor Revenue Forecast for 2026

- Forecast Upgrade: Omdia has raised its semiconductor revenue forecast for 2026 to 62.7%, reflecting unprecedented growth in the DRAM and NAND markets driven by sustained demand and ongoing supply shortages, with the DRAM market expected to nearly double in value and the NAND segment potentially quadrupling.

- Strong Enterprise Demand: In 2026, enterprises will implement a major server refresh cycle coinciding with exceptional hyperscaler capital expenditures, driving strong demand for data center servers and memory-intensive applications, with computing and data storage leading semiconductor revenue growth by 90% year-on-year, exceeding $700 billion.

- Positive Consumer Electronics Outlook: While smartphone unit shipments are expected to remain flat, semiconductor revenues will increase significantly due to higher memory pricing, with multiple flagship launches anticipated, including a new wave of foldables and AI-enabled high-end models, raising overall bill of materials costs.

- AI Demand Surge: The progression of AI applications has exponentially increased demand for memory and processing ICs, and while macroeconomic pressures and supply scaling challenges persist, current semiconductor revenue growth is primarily driven by higher average selling prices rather than unit shipment volumes, indicating unique industry dynamics.

See More

Informa TechTarget Drives B2B Market Transformation at Forrester Summit

- B2B Summit Presence: Informa TechTarget, as a Platinum sponsor of the 2026 Forrester B2B Summit, will showcase its GTM success strategies from April 26-29 in Phoenix, Arizona, which is expected to attract numerous industry participants and enhance brand visibility.

- AI-Driven Market Strategies: At the summit, Informa TechTarget's Travis Gonzalez will discuss how to optimize brand content through AI to improve brand discoverability and trust in the zero-click buyer journey, helping clients stand out in a competitive market.

- Collaboration with Tanium: Tanium's Katrina Ross will explore how aligning internal teams through precision data and integrated marketing strategies has significantly driven revenue pipeline growth, highlighting the importance of data-driven decision-making.

- Iron Mountain's Transformation Story: Iron Mountain's Mark Wiragh will share the success of its GTM transformation, emphasizing how the company has expanded from traditional records management into the digital records market, reflecting strategic adjustments and market adaptability in digital transformation.

See More

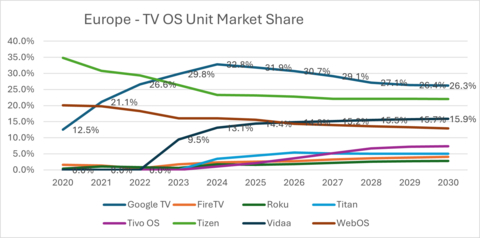

Forecast for European TV Operating Systems by 2030

- Market Share Shift: By 2030, TV operating systems that did not exist in 2022 are projected to control 28% of the European market, up from 21% in 2025, indicating a growing emphasis on advertising revenue among TV brands.

- Competitive Landscape Evolution: Google TV currently leads with a 32% market share but is expected to gradually lose ground to independent operating systems like VIDAA, Titan OS, and TiVo, which are reshaping the competitive dynamics in the European TV market.

- Revenue-Sharing Models: Unlike Google TV, VIDAA, Titan OS, and TiVo offer attractive revenue-sharing models that enable TV brands to earn ongoing income from home-screen ads and FAST channels, enhancing profit margins and competitive positioning.

- User Experience Control: These platforms provide manufacturers with greater control over user experience and viewer data, with Titan OS and TiVo integrating local broadcasters to deliver content that resonates better with traditional European viewing habits, thereby enhancing viewer engagement.

See More

Analysis of European TV Operating System Market Share

- Market Share Shift: By 2030, TV operating systems that did not exist in 2022 are projected to capture 28% of the European market, up from 21% in 2025, indicating a growing emphasis on advertising revenue by TV brands.

- Evolving Competitive Landscape: Google TV currently leads with a 32% market share but is expected to gradually lose ground to independent operating systems like VIDAA, Titan OS, and TiVo, which attract European manufacturers through active revenue-sharing models.

- User Experience Control: Unlike Google TV, VIDAA, Titan OS, and TiVo allow TV brands to maintain distinct brand identities and access to viewer data, enhancing user experience and aligning better with traditional European viewing habits.

- Strategic Partnerships: Titan OS and TiVo have formed a strategic ad-sales partnership in Europe, boosting their collective ad reach and making their revenue-sharing promises more appealing to TV brands, with a projected combined shipment of 11.9 million units by 2028.

See More

China's Cloud Infrastructure Market Continues Growth

- Market Growth: In Q4 2025, China's cloud infrastructure services spending reached $14.7 billion, marking a 26% year-on-year increase, indicating strong market recovery, with a forecasted growth rate of 26% for 2026, reflecting rising enterprise demand for cloud services.

- AI as Growth Driver: AI demand remains the primary growth driver, supporting not only model usage but also broader enterprise AI deployments, alongside rising demand for traditional cloud resources like compute, storage, and databases, indicating a shift in AI's role to a broader infrastructure demand driver.

- Key Vendor Developments: Alibaba Cloud maintained a 37% market share, launching products like Qwen3.5 and Wukong, achieving triple-digit year-on-year growth in AI-related revenue for ten consecutive quarters; Huawei Cloud and Tencent Cloud are also actively advancing their AI strategies to enhance market competitiveness.

- Ecosystem Collaboration: In Q4 2025, partner-driven cloud revenue accounted for 25% of the market, with expectations for further increases, highlighting the importance of ecosystem collaboration in the commercialization of AI, helping enterprises realize business value from AI adoption.

See More

Omdia Forecasts 62.7% Growth in Semiconductor Revenue by 2026

- Market Growth Forecast: Omdia projects a 62.7% increase in semiconductor revenue by 2026, driven primarily by rising memory chip prices and robust demand from AI and data center markets, with computing and data storage revenues expected to rise 90% year-over-year to over $700 billion.

- Memory Chip Demand: Demand for DRAM and NAND chips is anticipated to remain elevated, with the DRAM market nearly doubling in value by 2026 and the NAND segment potentially quadrupling from 2025 levels, highlighting the critical role of memory chips in AI servers.

- Supply Chain Challenges: Despite strong demand, conventional memory supplies remain constrained as manufacturers focus on producing higher-margin High Bandwidth Memory (HBM), with significant supply relief unlikely until 2027, impacting overall market dynamics.

- Risk Factors: Omdia notes that risks to the outlook include tariffs, energy costs, geopolitical tensions, and long-term returns on heavy AI infrastructure spending, which could negatively affect growth in the semiconductor industry.

See More

Omdia Significantly Raises Semiconductor Revenue Forecast for 2026

- Forecast Upgrade: Omdia has raised its semiconductor revenue forecast for 2026 to 62.7%, reflecting unprecedented growth in the DRAM and NAND markets driven by sustained demand and ongoing supply shortages, with the DRAM market expected to nearly double in value and the NAND segment potentially quadrupling.

- Strong Enterprise Demand: In 2026, enterprises will implement a major server refresh cycle coinciding with exceptional hyperscaler capital expenditures, driving strong demand for data center servers and memory-intensive applications, with computing and data storage leading semiconductor revenue growth by 90% year-on-year, exceeding $700 billion.

- Positive Consumer Electronics Outlook: While smartphone unit shipments are expected to remain flat, semiconductor revenues will increase significantly due to higher memory pricing, with multiple flagship launches anticipated, including a new wave of foldables and AI-enabled high-end models, raising overall bill of materials costs.

- AI Demand Surge: The progression of AI applications has exponentially increased demand for memory and processing ICs, and while macroeconomic pressures and supply scaling challenges persist, current semiconductor revenue growth is primarily driven by higher average selling prices rather than unit shipment volumes, indicating unique industry dynamics.

See More

Informa TechTarget Drives B2B Market Transformation at Forrester Summit

- B2B Summit Presence: Informa TechTarget, as a Platinum sponsor of the 2026 Forrester B2B Summit, will showcase its GTM success strategies from April 26-29 in Phoenix, Arizona, which is expected to attract numerous industry participants and enhance brand visibility.

- AI-Driven Market Strategies: At the summit, Informa TechTarget's Travis Gonzalez will discuss how to optimize brand content through AI to improve brand discoverability and trust in the zero-click buyer journey, helping clients stand out in a competitive market.

- Collaboration with Tanium: Tanium's Katrina Ross will explore how aligning internal teams through precision data and integrated marketing strategies has significantly driven revenue pipeline growth, highlighting the importance of data-driven decision-making.

- Iron Mountain's Transformation Story: Iron Mountain's Mark Wiragh will share the success of its GTM transformation, emphasizing how the company has expanded from traditional records management into the digital records market, reflecting strategic adjustments and market adaptability in digital transformation.

See More

Forecast for European TV Operating Systems by 2030

- Market Share Shift: By 2030, TV operating systems that did not exist in 2022 are projected to control 28% of the European market, up from 21% in 2025, indicating a growing emphasis on advertising revenue among TV brands.

- Competitive Landscape Evolution: Google TV currently leads with a 32% market share but is expected to gradually lose ground to independent operating systems like VIDAA, Titan OS, and TiVo, which are reshaping the competitive dynamics in the European TV market.

- Revenue-Sharing Models: Unlike Google TV, VIDAA, Titan OS, and TiVo offer attractive revenue-sharing models that enable TV brands to earn ongoing income from home-screen ads and FAST channels, enhancing profit margins and competitive positioning.

- User Experience Control: These platforms provide manufacturers with greater control over user experience and viewer data, with Titan OS and TiVo integrating local broadcasters to deliver content that resonates better with traditional European viewing habits, thereby enhancing viewer engagement.

See More

Analysis of European TV Operating System Market Share

- Market Share Shift: By 2030, TV operating systems that did not exist in 2022 are projected to capture 28% of the European market, up from 21% in 2025, indicating a growing emphasis on advertising revenue by TV brands.

- Evolving Competitive Landscape: Google TV currently leads with a 32% market share but is expected to gradually lose ground to independent operating systems like VIDAA, Titan OS, and TiVo, which attract European manufacturers through active revenue-sharing models.

- User Experience Control: Unlike Google TV, VIDAA, Titan OS, and TiVo allow TV brands to maintain distinct brand identities and access to viewer data, enhancing user experience and aligning better with traditional European viewing habits.

- Strategic Partnerships: Titan OS and TiVo have formed a strategic ad-sales partnership in Europe, boosting their collective ad reach and making their revenue-sharing promises more appealing to TV brands, with a projected combined shipment of 11.9 million units by 2028.

See More