CRK Overview

-

$

0.000

0.000(0.000%)

At close0.000(0.000%)Aft-market

ET

Loading chart...

The current price of CRK is 13.92 USD — it has decreased -1.83

Comstock Resources, Inc. is an independent natural gas producer operating primarily on the Haynesville shale, a natural gas basin located in North Louisiana and East Texas. The Company holds approximately 3,300 high-return net drilling locations in Haynesville and Bossier, including more than 2,500 locations in Western Haynesville. It includes over 535,000 net acre land positions in Western Haynesville in East Texas and drilling results confirming significant resource potential. Its operations are concentrated in Louisiana and Texas.

Wall Street analysts forecast CRK stock price to rise over the next 12 months. According to Wall Street analysts, the average 1-year price target for CRK is22.25 USD with a low forecast of 8.00 USD and a high forecast of 29.00 USD. However, analyst price targets are subjective and often lag stock prices, so investors should focus on the objective reasons behind analyst rating changes, which better reflect the company's fundamentals.

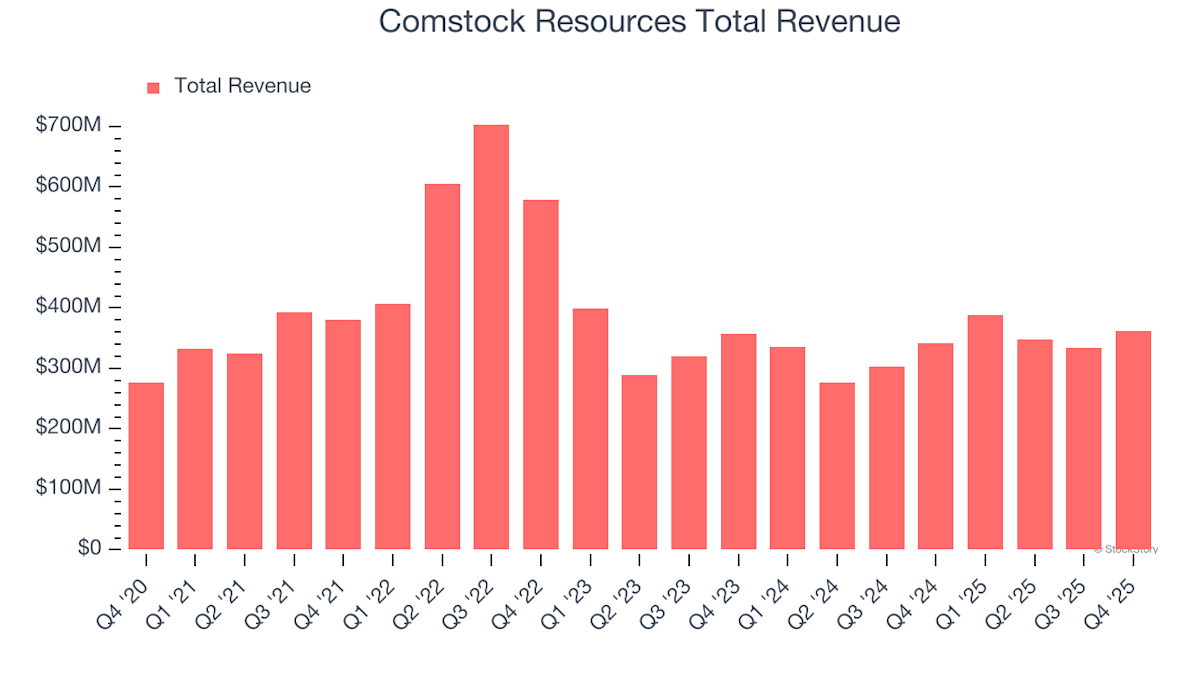

Comstock Resources Inc revenue for the last quarter amounts to 585.53M USD, increased 14.17

Comstock Resources Inc. EPS for the last quarter amounts to 0.37 USD, decreased -188.10

Comstock Resources Inc (CRK) has 252 emplpoyees as of July 09 2026.

Today CRK has the market capitalization of 4.09B USD.