Doximity Reports Strong Q3 2026 Earnings Amid Budget Uncertainties

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Feb 06 2026

0mins

Should l Buy DOCS?

Source: seekingalpha

- Significant Revenue Growth: Doximity reported Q3 revenue of $185.1 million, reflecting a 10% year-over-year increase and exceeding the high end of guidance by 2%, indicating strong performance and stable market demand in the healthcare sector.

- Innovative User Engagement: The company surpassed 3 million registered users, with 720,000 unique active prescribers, demonstrating Doximity's expanding influence among physicians and healthcare professionals, thereby enhancing its competitive position in the market.

- High AI Product Adoption: Over 300,000 unique prescribers utilized Doximity's AI products, with DocsGPT preferred at more than twice the rate of competitors, showcasing the company's leadership in AI and its potential for future growth.

- Cautious Future Outlook: While Q4 2026 revenue is expected to grow by 4%, management remains cautious due to policy uncertainties and increased AI infrastructure investments, emphasizing the strategy to leverage delayed client budget releases to drive future growth.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy DOCS?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on DOCS

Wall Street analysts forecast DOCS stock price to rise

18 Analyst Rating

14 Buy

4 Hold

0 Sell

Strong Buy

Current: 18.010

Low

25.00

Averages

42.75

High

63.00

Current: 18.010

Low

25.00

Averages

42.75

High

63.00

About DOCS

Doximity, Inc. operates as a digital platform for United States medical professionals. The Company provides an online platform which enables physicians and other healthcare professionals to collaborate with colleagues, stay up to date with the medical news and research, manage their careers and on-call schedules, streamline documentation and administrative paperwork, and conduct virtual patient visits. The Company's customers primarily include pharmaceutical companies and health systems that connect with healthcare professionals through the Company's digital Marketing, Hiring, and Workflow Solutions. Its marketing solutions provide customers to share content on the network. Its hiring solutions enable customers to identify, connect with, and hire from the network of both active and passive potential medical professional candidates. Its Workflow solutions allow customers to initiate voice and video calls with patients and manage on-call scheduling.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Doximity Reports Record Cash Flow in Q4, Exceeding Guidance

- Strong Financial Performance: Doximity reported $145 million in revenue for Q4 2026, a 5% year-over-year increase, with full-year revenue reaching $645 million, reflecting the company's robust growth potential in the market.

- Record Cash Flow: The company achieved a record $107 million in free cash flow during Q4, marking its first nine-digit free cash flow quarter, indicating significant improvements in operational efficiency and financial health.

- AI Investment Outlook: While minimal AI revenue contribution is expected for fiscal 2027, the company plans to increase spending on AI computing and go-to-market initiatives, demonstrating long-term confidence in AI technology's potential.

- Leadership Changes: The appointment of new CFO Matt Sonefeldt and new President Dr. Steve Zatz signifies a crucial adjustment in the executive team, aimed at driving the commercialization of AI Search and addressing market uncertainties.

See More

Bitcoin-Linked Stocks Rise as Starbucks Gets Upgrade

- Bitcoin-Linked Stocks Rise: Bitcoin rose 2% as the Senate Banking Committee discussed a regulatory framework for cryptocurrencies, with Coinbase shares jumping nearly 9%, indicating growing market confidence that could drive future growth for related companies.

- Starbucks Upgrade: TD Cowen upgraded Starbucks from hold to buy, raising its price target from $106 to $120, with analysts noting multiple positive sales drivers in a strong market backdrop, suggesting improved performance ahead.

- Ford Stock Surge: Ford shares rose 7%, adding to a 13% gain from Wednesday, as Morgan Stanley highlighted its energy storage business and partnership with CATL, projecting a $3 billion incremental revenue opportunity for Ford's Model e segment.

- Applied Materials Earnings Outlook: Applied Materials saw a 2% increase in shares ahead of its fiscal second-quarter results, with analysts expecting earnings of $2.66 per share and revenue of $7.68 billion, reflecting sustained optimism about semiconductor equipment demand.

See More

Doximity Shares Plunge 25% to Lowest Level Since IPO

- Disappointing Guidance: Doximity (DOCS) experienced a ~25% drop in stock price after its Q4 fiscal 2026 guidance failed to meet Wall Street expectations, reaching its lowest level since its 2021 IPO, indicating market concerns over future growth.

- Analyst Downgrade: KeyBanc Capital Markets downgraded Doximity from Overweight to Sector Weight, projecting fiscal 2027 revenue between $664 million and $676 million due to the AI Search product missing the sales peak, highlighting a lack of catalysts and increased downside risk.

- Market Share Challenges: Analyst Scott Schoenhaus noted that Doximity is not gaining market share this year as budget managers prefer cutting-edge AI or low-cost options over its premium offerings, reflecting a more competitive market landscape.

- AI Investment Year: While Doximity is catching up in AI, the anticipated revenue from the AI Search product is not expected until the second half of 2027, putting pressure on the company's growth outlook and indicating insufficient competitiveness in the digital advertising market.

See More

Doximity Shares Drop 24% After Disappointing Q4 Earnings Report

- Disappointing Performance: Doximity's Q4 sales rose by 5% and free cash flow (FCF) increased by 11%, yet the company fell short of Wall Street's earnings expectations, resulting in a 24% drop in share price as of Thursday morning.

- Conservative Future Outlook: Management's full-year revenue growth guidance for 2027 is only 3% to 5%, coupled with a declining adjusted EBITDA margin, indicating significant growth challenges ahead for the company.

- Increased AI Investment: Despite profitability pressures, Doximity is ramping up investments in AI products, which are expected to further impact margins; however, the company is making promising strides in technology adoption.

- Stable Market Position: With 85% of U.S. physicians on its network and partnerships with 20 of the top hospitals and pharmaceutical companies, Doximity's leadership remains intact, although the industry slowdown will still pose challenges.

See More

Key Market Highlights for Today

- Cerebras IPO: Cerebras Systems successfully raised $5.5 billion in its IPO today, focusing on ultra-fast AI chip processing, with OpenAI committing to purchase its computing capacity, indicating strong market demand for efficient AI computing.

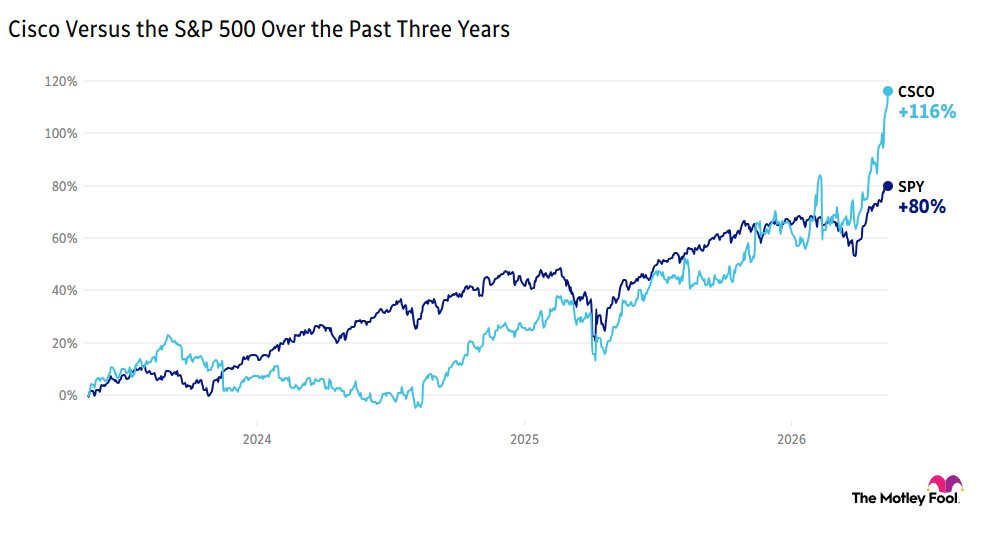

- Cisco's Strong Quarter: Cisco reported a blowout quarter with robust data center performance, sending shares up nearly 15% in premarket trading, reflecting massive demand for networking equipment and underscoring the ongoing growth in AI spending, enhancing the investment case for data center stocks.

- Dell Price Target Increase: Citi raised Dell's price target from $235 to $290 ahead of its earnings report, anticipating continued strong performance in the server market; despite rising memory costs, Dell's scale and pricing agility are expected to provide competitive advantages.

- Broadcom Price Target Boost: Wells Fargo increased Broadcom's price target from $430 to $545, significantly raising AI chip revenue forecasts, highlighting the underappreciated potential in its networking segment, which could drive stock price appreciation.

See More

Cisco's Transformation in the AI Era

- Earnings Surge: Cisco (CSCO) saw a 20% pre-market jump, driven by a positive outlook from its business restructuring, with CFO Mark Patterson indicating an expansion of its silicon portfolio to meet data center demands, thereby enhancing its competitive edge in the AI market.

- Job Cuts and Investments: CEO Chuck Robbins announced nearly 4,000 job cuts; however, the company plans to increase investments in AI, aiming to shift resources towards areas with the strongest demand and long-term value creation, ensuring sustainable growth in the future.

- Chinese Market Opportunities: Alibaba (BABA) and JD.com (JD) received U.S. approval to purchase Nvidia's H200 chips, although no deliveries have been made yet, indicating a significant potential revenue opportunity for Nvidia in the Chinese market, which could impact its dominance in the global chip market.

- AI-Driven Growth: Cellebrite DI (CLBT) is expected to report an 18% year-over-year revenue growth, primarily driven by strong demand for AI-driven investigative tools, showcasing the company's robust execution and adaptability in the AI sector.

See More

Doximity Reports Record Cash Flow in Q4, Exceeding Guidance

- Strong Financial Performance: Doximity reported $145 million in revenue for Q4 2026, a 5% year-over-year increase, with full-year revenue reaching $645 million, reflecting the company's robust growth potential in the market.

- Record Cash Flow: The company achieved a record $107 million in free cash flow during Q4, marking its first nine-digit free cash flow quarter, indicating significant improvements in operational efficiency and financial health.

- AI Investment Outlook: While minimal AI revenue contribution is expected for fiscal 2027, the company plans to increase spending on AI computing and go-to-market initiatives, demonstrating long-term confidence in AI technology's potential.

- Leadership Changes: The appointment of new CFO Matt Sonefeldt and new President Dr. Steve Zatz signifies a crucial adjustment in the executive team, aimed at driving the commercialization of AI Search and addressing market uncertainties.

See More

Bitcoin-Linked Stocks Rise as Starbucks Gets Upgrade

- Bitcoin-Linked Stocks Rise: Bitcoin rose 2% as the Senate Banking Committee discussed a regulatory framework for cryptocurrencies, with Coinbase shares jumping nearly 9%, indicating growing market confidence that could drive future growth for related companies.

- Starbucks Upgrade: TD Cowen upgraded Starbucks from hold to buy, raising its price target from $106 to $120, with analysts noting multiple positive sales drivers in a strong market backdrop, suggesting improved performance ahead.

- Ford Stock Surge: Ford shares rose 7%, adding to a 13% gain from Wednesday, as Morgan Stanley highlighted its energy storage business and partnership with CATL, projecting a $3 billion incremental revenue opportunity for Ford's Model e segment.

- Applied Materials Earnings Outlook: Applied Materials saw a 2% increase in shares ahead of its fiscal second-quarter results, with analysts expecting earnings of $2.66 per share and revenue of $7.68 billion, reflecting sustained optimism about semiconductor equipment demand.

See More

Doximity Shares Plunge 25% to Lowest Level Since IPO

- Disappointing Guidance: Doximity (DOCS) experienced a ~25% drop in stock price after its Q4 fiscal 2026 guidance failed to meet Wall Street expectations, reaching its lowest level since its 2021 IPO, indicating market concerns over future growth.

- Analyst Downgrade: KeyBanc Capital Markets downgraded Doximity from Overweight to Sector Weight, projecting fiscal 2027 revenue between $664 million and $676 million due to the AI Search product missing the sales peak, highlighting a lack of catalysts and increased downside risk.

- Market Share Challenges: Analyst Scott Schoenhaus noted that Doximity is not gaining market share this year as budget managers prefer cutting-edge AI or low-cost options over its premium offerings, reflecting a more competitive market landscape.

- AI Investment Year: While Doximity is catching up in AI, the anticipated revenue from the AI Search product is not expected until the second half of 2027, putting pressure on the company's growth outlook and indicating insufficient competitiveness in the digital advertising market.

See More

Doximity Shares Drop 24% After Disappointing Q4 Earnings Report

- Disappointing Performance: Doximity's Q4 sales rose by 5% and free cash flow (FCF) increased by 11%, yet the company fell short of Wall Street's earnings expectations, resulting in a 24% drop in share price as of Thursday morning.

- Conservative Future Outlook: Management's full-year revenue growth guidance for 2027 is only 3% to 5%, coupled with a declining adjusted EBITDA margin, indicating significant growth challenges ahead for the company.

- Increased AI Investment: Despite profitability pressures, Doximity is ramping up investments in AI products, which are expected to further impact margins; however, the company is making promising strides in technology adoption.

- Stable Market Position: With 85% of U.S. physicians on its network and partnerships with 20 of the top hospitals and pharmaceutical companies, Doximity's leadership remains intact, although the industry slowdown will still pose challenges.

See More

Key Market Highlights for Today

- Cerebras IPO: Cerebras Systems successfully raised $5.5 billion in its IPO today, focusing on ultra-fast AI chip processing, with OpenAI committing to purchase its computing capacity, indicating strong market demand for efficient AI computing.

- Cisco's Strong Quarter: Cisco reported a blowout quarter with robust data center performance, sending shares up nearly 15% in premarket trading, reflecting massive demand for networking equipment and underscoring the ongoing growth in AI spending, enhancing the investment case for data center stocks.

- Dell Price Target Increase: Citi raised Dell's price target from $235 to $290 ahead of its earnings report, anticipating continued strong performance in the server market; despite rising memory costs, Dell's scale and pricing agility are expected to provide competitive advantages.

- Broadcom Price Target Boost: Wells Fargo increased Broadcom's price target from $430 to $545, significantly raising AI chip revenue forecasts, highlighting the underappreciated potential in its networking segment, which could drive stock price appreciation.

See More

Cisco's Transformation in the AI Era

- Earnings Surge: Cisco (CSCO) saw a 20% pre-market jump, driven by a positive outlook from its business restructuring, with CFO Mark Patterson indicating an expansion of its silicon portfolio to meet data center demands, thereby enhancing its competitive edge in the AI market.

- Job Cuts and Investments: CEO Chuck Robbins announced nearly 4,000 job cuts; however, the company plans to increase investments in AI, aiming to shift resources towards areas with the strongest demand and long-term value creation, ensuring sustainable growth in the future.

- Chinese Market Opportunities: Alibaba (BABA) and JD.com (JD) received U.S. approval to purchase Nvidia's H200 chips, although no deliveries have been made yet, indicating a significant potential revenue opportunity for Nvidia in the Chinese market, which could impact its dominance in the global chip market.

- AI-Driven Growth: Cellebrite DI (CLBT) is expected to report an 18% year-over-year revenue growth, primarily driven by strong demand for AI-driven investigative tools, showcasing the company's robust execution and adaptability in the AI sector.

See More