Vertex Pharmaceuticals' Suzetrigine New Drug Submission Accepted for Review by Health Canada

Vertex Pharmaceuticals announced that Health Canada has accepted for review a New Drug Submission for suzetrigine for the treatment of moderate-to-severe acute pain in adults. Suzetrigine is a selective NaV1.8 pain signal inhibitor that represents a new class of oral pain medicine; it is not an opioid or a nonsteroidal anti-inflammatory drug. If approved by Health Canada, suzetrigine has the potential to be the first new class of medicine in Canada to treat acute pain in over twenty years. Vertex intends for the regulatory review of suzetrigine to be part of an aligned review with Canadian Health Technology Assessment organizations: Canada's Drug Agency and the Institut national d'excellence en sante et en services sociaux in Quebec. Aligned reviews provide an opportunity for information sharing between Health Canada and HTA bodies, leading to greater coordination to support Canadians' timely access to effective new therapies.

Trade with 70% Backtested Accuracy

Analyst Views on VRTX

About VRTX

About the author

CRISPR Therapeutics Shows Promising Upside Potential

- Strong Stock Performance: CRISPR Therapeutics' shares have surged 56% over the past year, significantly outperforming the S&P 500's 30% gain, indicating robust market confidence in its growth prospects.

- Optimistic Analyst Targets: According to Yahoo! Finance, CRISPR's average price target is $82.55, suggesting nearly 51% upside from current levels, while Piper Sandler's analyst has set a target of $110, indicating the stock could potentially double in the next 12 months.

- Catalysts from Clinical Trials: The ongoing development of the anticoagulant CTX611 could yield crucial clinical trial data in the coming months, targeting a $20 billion market, and positive results could significantly boost the stock price.

- Market Expansion Potential: The Casgevy drug, developed in collaboration with Vertex Pharmaceuticals, has yet to generate significant sales despite its 2023 approval due to its complex administration and high cost; however, the recent request for approval for children aged 5 to 11 could greatly expand its market potential, with annual revenues expected to exceed $1 billion in the coming years.

Vertex Pharmaceuticals Set to Announce Q2 Earnings on May 11

- Earnings Announcement: Vertex Pharmaceuticals is set to release its Q2 2023 earnings report on May 11 after market close, with consensus EPS estimate at $4.75, reflecting a 5.1% year-over-year increase, and revenue estimate at $3.22 billion, up 8.8% year-over-year.

- Historical Performance Review: Over the past two years, Vertex has exceeded EPS estimates 50% of the time and revenue estimates 63% of the time, indicating a degree of stability in its financial performance amidst market fluctuations.

- Expectation Adjustment Dynamics: In the last three months, EPS estimates have seen 2 upward revisions and 9 downward revisions, while revenue estimates experienced 8 upward revisions and 4 downward revisions, reflecting market uncertainty regarding the company's future performance.

- Long-term Revenue Outlook: Vertex projects revenue for 2026 to be between $12.95 billion and $13.1 billion, while targeting over $500 million from non-CF products, showcasing the company's strategic focus on diversifying its product lines.

Vertex Pharmaceuticals: Investment Returns and Future Outlook

- Significant Investment Returns: An investment of $20,000 in Vertex Pharmaceuticals during its 1991 IPO would now exceed $1 million, reflecting a commendable 14% compound annual growth rate, which outperforms the S&P 500's 11% over the same period, indicating the company's robust long-term growth potential.

- Core Market Dominance: Vertex Pharmaceuticals leads the cystic fibrosis (CF) market, treating approximately 95% of CF patients in the U.S., although its revenue growth has slowed, with an 8% year-over-year increase to $2.99 billion in Q1, suggesting sustained market demand despite challenges.

- Diversification Challenges: While Vertex aims to reduce its reliance on CF, it anticipates $500 million in non-CF revenue this year, a significant increase from $10 million in 2024, yet this growth remains insufficient, highlighting ongoing challenges in its diversification efforts.

- Future Growth Potential: Vertex is seeking approval for Casgevy, a gene-editing drug for sickle cell disease and transfusion-dependent beta-thalassemia, which could drive future growth, alongside advancing povetacicept for IgA nephropathy, showcasing the potential for an expanded product portfolio.

Vertex Pharmaceuticals' Future Outlook Appears Promising

- Core Business Slowdown: Vertex Pharmaceuticals reported an 8% year-over-year revenue increase to $2.99 billion in Q1, which, while not terrible, reflects a general downward trend in growth over recent years, indicating weakness in its core market.

- Non-CF Revenue Potential: The company expects at least $500 million in non-CF revenue for 2023, a significant increase from $10 million in 2024, suggesting that its diversification efforts are beginning to pay off.

- New Drug Development Progress: Vertex is seeking approval for Casgevy, a gene-editing medicine for sickle cell disease and transfusion-dependent beta-thalassemia, aimed at providing early treatment for patients aged 5 to 11, highlighting its significant market potential.

- Future Growth Outlook: As Vertex continues to develop new products in the CF space and expand its portfolio, it is expected to achieve stronger revenue and earnings growth in the coming years, presenting a positive long-term outlook.

Vertex Pharmaceuticals Confident in Renal Franchise

- Renal Business Outlook: Vertex Pharmaceuticals (VRTX) management expresses strong confidence in its emerging renal franchise, indicating that the strategic positioning in this area is beginning to yield results, which is expected to drive future revenue growth.

- Market Potential: With the increasing global demand for treatments for kidney diseases, Vertex's renal product line is poised to capture significant market share in the coming years, thereby enhancing the company's overall competitiveness.

- R&D Investment: The company continues to increase its investment in research and development related to kidney diseases, aiming to meet unmet medical needs through innovative therapies, further solidifying its leadership position in the biopharmaceutical industry.

- Management Confidence: The management's confidence reflects a positive assessment of product development progress, which is expected to attract more investor attention and improve the company's performance in the capital markets.

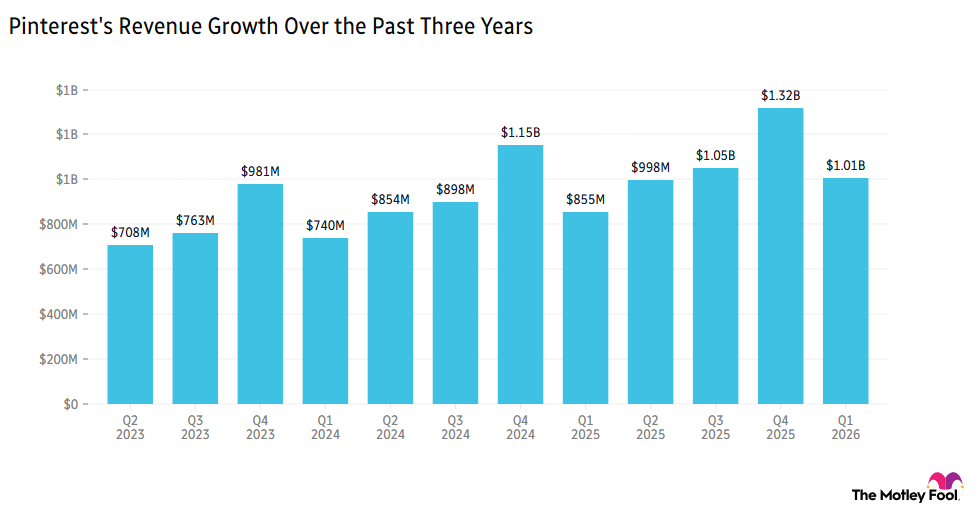

Pinterest Surges on Record User Growth and Positive Revenue Guidance

- Strong User Growth: Pinterest (PINS) surged over 15% ahead of market open, driven by an 11% year-over-year increase in monthly active users (MAU), marking the tenth consecutive quarter of double-digit growth, indicating that enhanced user engagement will support future profitability.

- Optimistic Revenue Guidance: Pinterest's revenue guidance exceeded expectations, with CEO Bill Ready emphasizing the company's commitment to aligning profitability with user engagement, thereby boosting investor confidence and driving stock price increases.

- Positive Market Reaction: Analyst Rich Greifner highlighted that Pinterest's large and engaged user base, characterized by high commercial intent, makes it an attractive platform for advertisers, further solidifying its competitive position in the advertising market.

- Favorable Industry Outlook: As Pinterest's user growth and revenue expectations improve, market confidence in its future performance is likely to attract more investor interest, propelling further development in the social media sector.

CRISPR Therapeutics Shows Promising Upside Potential

- Strong Stock Performance: CRISPR Therapeutics' shares have surged 56% over the past year, significantly outperforming the S&P 500's 30% gain, indicating robust market confidence in its growth prospects.

- Optimistic Analyst Targets: According to Yahoo! Finance, CRISPR's average price target is $82.55, suggesting nearly 51% upside from current levels, while Piper Sandler's analyst has set a target of $110, indicating the stock could potentially double in the next 12 months.

- Catalysts from Clinical Trials: The ongoing development of the anticoagulant CTX611 could yield crucial clinical trial data in the coming months, targeting a $20 billion market, and positive results could significantly boost the stock price.

- Market Expansion Potential: The Casgevy drug, developed in collaboration with Vertex Pharmaceuticals, has yet to generate significant sales despite its 2023 approval due to its complex administration and high cost; however, the recent request for approval for children aged 5 to 11 could greatly expand its market potential, with annual revenues expected to exceed $1 billion in the coming years.

Vertex Pharmaceuticals Set to Announce Q2 Earnings on May 11

- Earnings Announcement: Vertex Pharmaceuticals is set to release its Q2 2023 earnings report on May 11 after market close, with consensus EPS estimate at $4.75, reflecting a 5.1% year-over-year increase, and revenue estimate at $3.22 billion, up 8.8% year-over-year.

- Historical Performance Review: Over the past two years, Vertex has exceeded EPS estimates 50% of the time and revenue estimates 63% of the time, indicating a degree of stability in its financial performance amidst market fluctuations.

- Expectation Adjustment Dynamics: In the last three months, EPS estimates have seen 2 upward revisions and 9 downward revisions, while revenue estimates experienced 8 upward revisions and 4 downward revisions, reflecting market uncertainty regarding the company's future performance.

- Long-term Revenue Outlook: Vertex projects revenue for 2026 to be between $12.95 billion and $13.1 billion, while targeting over $500 million from non-CF products, showcasing the company's strategic focus on diversifying its product lines.

Vertex Pharmaceuticals: Investment Returns and Future Outlook

- Significant Investment Returns: An investment of $20,000 in Vertex Pharmaceuticals during its 1991 IPO would now exceed $1 million, reflecting a commendable 14% compound annual growth rate, which outperforms the S&P 500's 11% over the same period, indicating the company's robust long-term growth potential.

- Core Market Dominance: Vertex Pharmaceuticals leads the cystic fibrosis (CF) market, treating approximately 95% of CF patients in the U.S., although its revenue growth has slowed, with an 8% year-over-year increase to $2.99 billion in Q1, suggesting sustained market demand despite challenges.

- Diversification Challenges: While Vertex aims to reduce its reliance on CF, it anticipates $500 million in non-CF revenue this year, a significant increase from $10 million in 2024, yet this growth remains insufficient, highlighting ongoing challenges in its diversification efforts.

- Future Growth Potential: Vertex is seeking approval for Casgevy, a gene-editing drug for sickle cell disease and transfusion-dependent beta-thalassemia, which could drive future growth, alongside advancing povetacicept for IgA nephropathy, showcasing the potential for an expanded product portfolio.

Vertex Pharmaceuticals' Future Outlook Appears Promising

- Core Business Slowdown: Vertex Pharmaceuticals reported an 8% year-over-year revenue increase to $2.99 billion in Q1, which, while not terrible, reflects a general downward trend in growth over recent years, indicating weakness in its core market.

- Non-CF Revenue Potential: The company expects at least $500 million in non-CF revenue for 2023, a significant increase from $10 million in 2024, suggesting that its diversification efforts are beginning to pay off.

- New Drug Development Progress: Vertex is seeking approval for Casgevy, a gene-editing medicine for sickle cell disease and transfusion-dependent beta-thalassemia, aimed at providing early treatment for patients aged 5 to 11, highlighting its significant market potential.

- Future Growth Outlook: As Vertex continues to develop new products in the CF space and expand its portfolio, it is expected to achieve stronger revenue and earnings growth in the coming years, presenting a positive long-term outlook.

Vertex Pharmaceuticals Confident in Renal Franchise

- Renal Business Outlook: Vertex Pharmaceuticals (VRTX) management expresses strong confidence in its emerging renal franchise, indicating that the strategic positioning in this area is beginning to yield results, which is expected to drive future revenue growth.

- Market Potential: With the increasing global demand for treatments for kidney diseases, Vertex's renal product line is poised to capture significant market share in the coming years, thereby enhancing the company's overall competitiveness.

- R&D Investment: The company continues to increase its investment in research and development related to kidney diseases, aiming to meet unmet medical needs through innovative therapies, further solidifying its leadership position in the biopharmaceutical industry.

- Management Confidence: The management's confidence reflects a positive assessment of product development progress, which is expected to attract more investor attention and improve the company's performance in the capital markets.

Pinterest Surges on Record User Growth and Positive Revenue Guidance

- Strong User Growth: Pinterest (PINS) surged over 15% ahead of market open, driven by an 11% year-over-year increase in monthly active users (MAU), marking the tenth consecutive quarter of double-digit growth, indicating that enhanced user engagement will support future profitability.

- Optimistic Revenue Guidance: Pinterest's revenue guidance exceeded expectations, with CEO Bill Ready emphasizing the company's commitment to aligning profitability with user engagement, thereby boosting investor confidence and driving stock price increases.

- Positive Market Reaction: Analyst Rich Greifner highlighted that Pinterest's large and engaged user base, characterized by high commercial intent, makes it an attractive platform for advertisers, further solidifying its competitive position in the advertising market.

- Favorable Industry Outlook: As Pinterest's user growth and revenue expectations improve, market confidence in its future performance is likely to attract more investor interest, propelling further development in the social media sector.